The fighting in Iran is about to enter its third month with no clear end in sight.

While reports state that a deal is being made that would lead to the reopening of the Strait of Hormuz, it’s still uncertain whether it will happen, given the complexities surrounding any form of a deal or truce.

Hormuz is a vital transport lane, as 20% of global oil supplies and a big volume of liquefied natural gas (“LNG”) pass through it daily.

While a surge in crude oil prices is the most immediate effect of the conflict, it also has broader ramifications for the economy and other industries.

Crude oil and other substances extracted from fossil fuels aren’t just refined for energy use. Petroleum is a raw material that’s used in the creation of various products such as fertilizers, polyurethane, solvents, plastics, and other end-user products.

Given the reliance and exposure of multiple industries to oil, the effects of the conflict have been mixed. While some firms have benefitted from the supply crunch and elevated prices, the prospects of others have worsened.

Unfortunately, Hasbro (HAS) belongs to the latter group.

Hasbro is a games and toymaking company. For years, it has manufactured toys and other entertainment products based on various intellectual properties (“IPs”) which includes the likes of Transformers, Power Rangers, G.I. Joe, Nerf, Play-Doh, Star Wars, and Marvel, to name a few. It also owns the popular board game Monopoly.

The company’s revenues for years have been drawn from toy sales based on licensed IPs. However, in recent years, it has targeted consumers in older age brackets through the collectibles category, of which Magic: The Gathering and Dungeons & Dragons serve as the flagship offerings.

Hasbro reported its earnings for Q1 2026 last week.

The company posted a 12.7% year-over-year rise in revenue for Q1, driven primarily by sales from its Wizards and Digital Gaming segment. However, this growth was dragged down by flat sales figures in traditional toys and a decline in its Entertainment segment.

As a result, the $1 billion quarterly revenue it reported narrowly missed consensus estimates.

Hasbro’s management also expressed a moderate, if not outright conservative, outlook. The company maintained its 3% to 5% forecast for the rest of 2026. Analyst forecasts for sales growth were set at around 5%.

The toymaker’s outlook indicates that it’s anticipating slower growth due to high oil prices, tariff concerns, and the yet-to-be-determined cost of a recent cybersecurity breach.

As a result, Hasbro’s stock is down by nearly 8%.

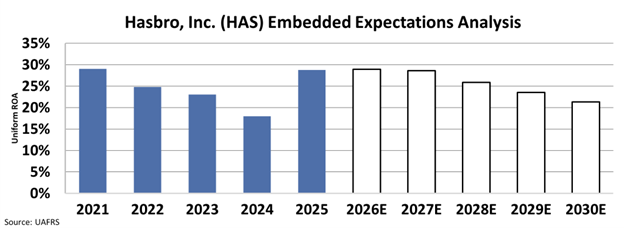

Uniform Accounting validates the investor response to Hasbro’s most recent quarter. And we can see this through our Embedded Expectations Analysis (“EEA”) framework.

We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Hasbro delivered a Uniform return on assets (“ROA”) of 29% last year. However, by 2030, returns are expected to drop to 21%.

Hasbro, due to its reliance on plastics for a vast swath of its products, is exposed to the effects of oil price volatility. As long as oil prices continue to remain elevated, the company will continue to face rising costs and headwinds, consequently harming its near- and long-term prospects.

And as long as conflict, geopolitical uncertainty, and tensions continue to wreak havoc in the Middle East, it may be best to stay away from the company for now.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.