Money market funds emerged as a notable beneficiary of the collapse of Silicon Valley Bank. While much has been said about depositors shifting their money from regional banks to larger, more established banks, little attention has been given to the consistent movement of deposits from banks to money market funds over the past few quarters. In today’s FA Alpha Daily, we’ll take a closer look at money market funds and see how they have benefited more than the big banks from the recent banking crisis.

FA Alpha Daily:

Monday Macro

Powered by Valens Research

This move is going to have a big impact on the economy in the coming quarters.

We talked last week about how commercial and industrial (“C&I”) loan growth had already turned negative before the bank failures.

These loans are not given to individuals. They provide companies with funds so they can invest and grow. That is why it is an incredibly important metric to watch to understand the overall health of the economy.

C&I loans dropping means companies have less cash at hand to spend, possibly leading to a slowdown in the economy.

Part of the reason why that dropped was because of another metric we watch, called the Senior Loan Officer Opinion Survey (“SLOOS”). It shows how willing banks are to make loans.

It turns out, banks were already aggressively tightening lending standards way before the Silicon Valley Bank collapse.

To complete the SLOOS, every quarter Fed regulators go out and survey loan officers, asking them if they’re making it easier or harder for corporates and consumers to get access to credit.

According to the survey, a significant share of banks reported tightened standards on C&I loans to firms of all sizes as 2022 ended. Banks charged higher premiums on riskier loans, spreads over the cost of funds increased and covenants and collateralization requirements were tightened.

Again, that was before Silicon Valley Bank collapsed and many regional banks experienced a depositor run.

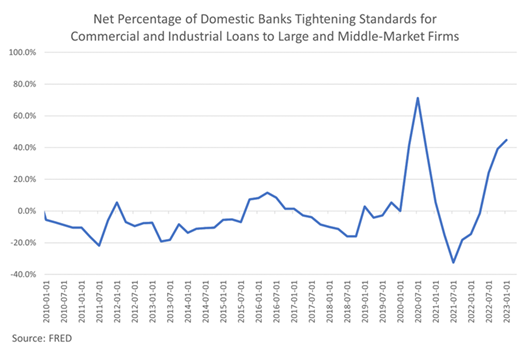

The chart below shows the percentage of domestic banks that tightened standards for C&I loans to large and middle-market firms.

The percentage has been increasing pretty quickly since July 2021.

The rush to money market is going to make this lending freeze much worse.

Regional banks are a vital part of the lending ecosystem. They do much more to lend to local businesses, commercial real estate, and to create mortgages, than big banks and money market funds do.

After all, money markets just fund very short-term borrowing from corporations, nothing long enough to allow for lasting investment.

As regional bank deposits have been shrinking, that limits the amount of loans these banks can make.

And that means they are going to get more and more selective about which loans they underwrite. It’s no surprise that as far as the SLOOS is concerned, the first quarter was one of the fastest rates of tightening we’ve seen in a long time.

The first quarter data was just published, and 45% of banks tightened lending standards. That might not look like much of an increase from the fourth quarter data. That misunderstands the data though.

What this data means is 45% of banks tightened lending standards from what their lending standards already were in the fourth quarter.

So it’s not that lending got slightly tighter in the past three months. A lot of banks tightened even more than they had before.

The only time that banks tightened faster than this in the past 10 years was in the third quarter of 2020, in the midst of the pandemic. At the time everyone was still terrified companies were going to go under left and right.

If the only time in the past decade that credit has been getting tighter faster than it is today was in the midst of the pandemic, you know credit is getting a lot tougher to come by.

As we’ve talked about time and time again, credit cycles lead economic cycles.

And so if credit is getting much harder for corporates and consumers to come by, that is going to continue to push us further and further towards a recession. And at a faster rate than we would have expected before.

All the more reason to continue to be very cautious with your investments right now.

Don’t let the recent strength in the market fool you. Until credit starts to flow more easily, we’re not in a new bull market. We continue to be in a choppy sideways market where you need to be tactical to keep your head above water.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

To see our best macro insights, become an FA Alpha and get access to FA Alpha Pulse.