Fear isn’t always rational. In general, the market tends to get spooked by rising interest rates since it dislikes rapid changes in the monetary landscape.

For instance, Bloomberg’s “Era of Ultra-Cheap Money Begins to Fade in Corporate Bond Market” asserts that the last decade has been great for companies looking to refinance debt, but this trend is coming to a close post-pandemic with the increase in borrowing costs.

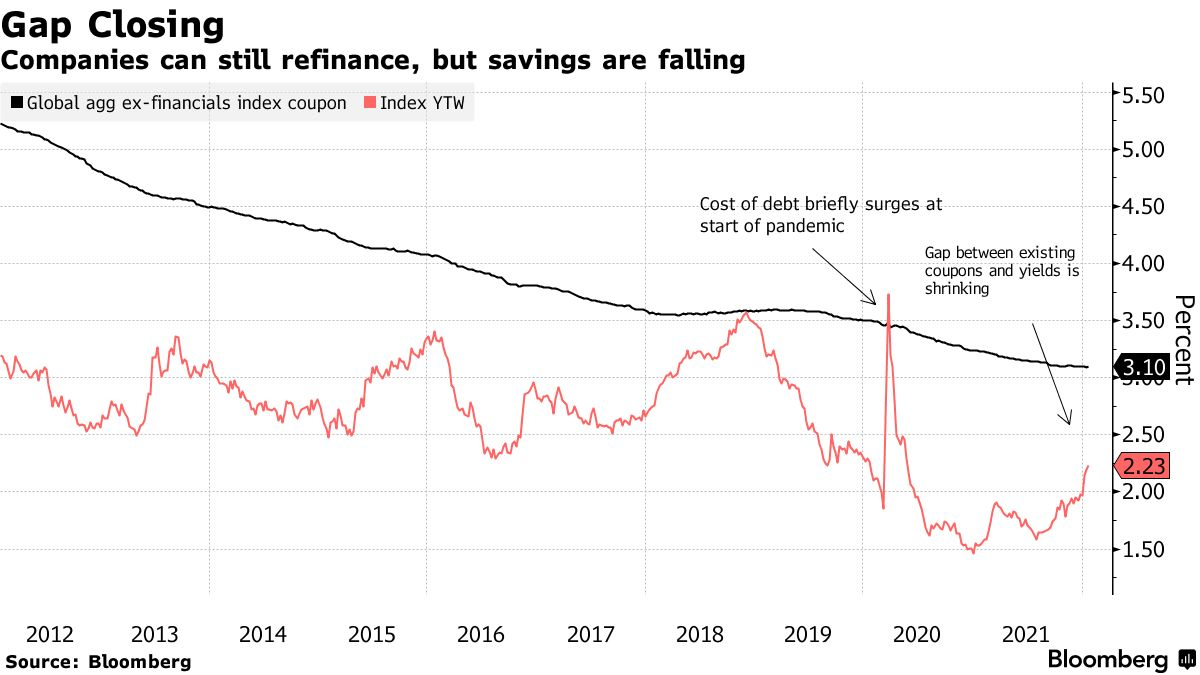

For the past decade, the coupon rates companies paid out on their debt have been higher than the prevailing cost to borrow. This encouraged companies to refinance their debt to lower their aggregate cost of capital.

In other words, it became easier for companies to take on debt to fund operations or expansion efforts.

The chart below compares coupon cost (the black line) with the cost of debt (the red line).

In the chart, we can see the first time the cost to refinance flirted with the current coupon cost for companies was in late 2018, when the market was tumbling. The second was in March 2020, during the onset of the pandemic, when the cost of debt briefly surged and crossed the line before retreating to much lower levels.

Most recently, the cost of debt appears to be closing in on the coupon rate, which draws concerns for what that could mean for companies.

However, the change in costs isn’t as important to companies refinancing as the absolute value of the borrowing cost.

While the spread between the coupon and borrowing cost has tightened by about 0.15% to 0.2% since late 2021 when the Federal Reserve started raising rates, it is still about 0.9%.

But even if the Fed were to raise rates by 1% in 2022, there would probably still be a 0.2% to 0.3% spread between the cost to refinance and the coupon cost of debt.

+++++++++++++

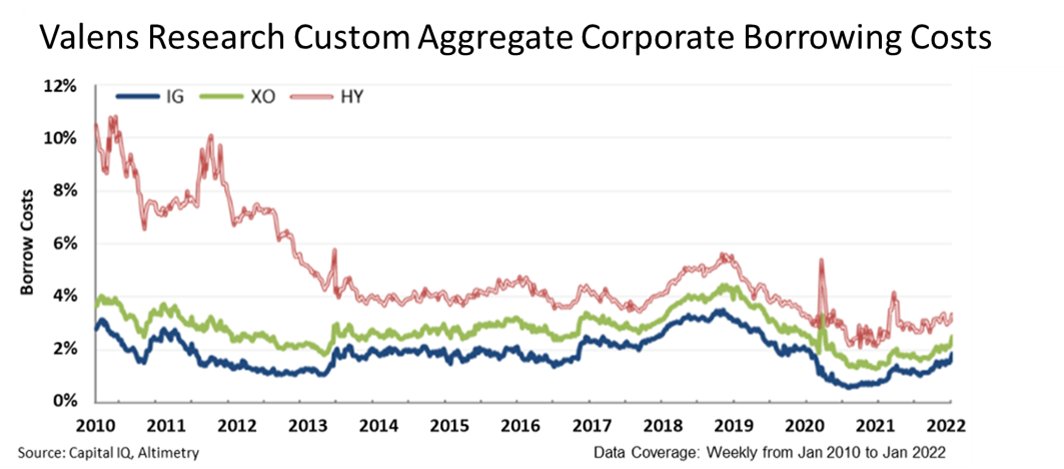

The chart highlights the total cost of U.S. corporations to borrow. We break it down into three buckets: investment grade (“IG”), crossover (“XO”), and high yield (“HY”).

IG companies are among the largest, safest, and most stable public companies, while HY companies are the smallest and riskiest. So, it makes sense that HY cost to borrow is always more expensive than IG, and XO charts toward the middle.

After the brief spike in 2020 at the start of the pandemic, the cost to borrow returned to incredibly low levels thanks to wide-open credit markets.

Right now, we see that the cost to borrow remains at very low levels for HY, IG, and XO companies.

Because the rates are so low, even if the cost to refinance rose 1%, it would just be in line with normal levels from the past decade, where we experienced strong positive economic growth.

Companies still have room to grow and refinance without overly rising debt burdens.

While there may be concerns about the closing gap of aggregate borrowing costs, there is still plenty of room for growth.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

To see our best macro insights, get access to FA Alpha Pulse.