FA Alpha Daily

Powered by Valens Research

In 2024, the semiconductor industry experienced solid growth driven by increased demand from data centers.

The surge in spending on GPUs and AI processors helped propel overall revenue, as data centers emerged as the second-largest market for chips behind smartphones, now aiming for the top spot.

This shift was fueled by a growing need to support AI workloads, prompting many companies to invest in advanced computing solutions and AI infrastructure.

While most of the semiconductor companies like Nvidia (NVDA) and Broadcom (AVGO) had reaped the rewards of the AI investments and experienced surges in their stock prices, one giant in this space struggled severely.

Intel (INTC) has faced a challenging year, missing out on growth that many other semiconductor companies have enjoyed.

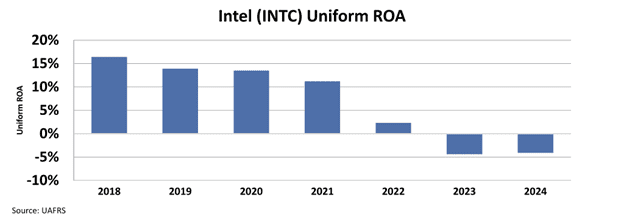

The company’s Uniform return on assets ”ROA” fell to around (5%) while its struggles have been compounded by internal turmoil and strategic missteps.

However, the appointment of a new CEO, Lip-Bu Tan, has sparked optimism among investors and industry watchers, signaling a potential turning point for the embattled chipmaker.

Tan’s appointment comes after a period of uncertainty following the abrupt retirement of former CEO Pat Gelsinger in December 2024.

Gelsinger’s departure raised concerns about Intel’s future, especially as the company grappled with declining market share and intense competition from rivals like Nvidia, AMD, and TSMC.

Tan, who led Cadence for 12 years before stepping down in 2021, brings a wealth of experience in the semiconductor industry.

His return to Intel, where he previously served on the board, has been met with cautious optimism, with stock surging more than 10% after the announcement.

The company has been criticized for its risk-averse culture, bloated workforce, and lagging strategy in key areas like AI.

Tan himself reportedly left Intel’s board in August due to concerns about the company’s turnaround plan.

He was particularly vocal about the need to streamline operations and reduce the influence of middle managers, whom he believed were hindering progress in critical divisions like server and desktop chips.

Intel has already taken steps to address some of these issues. In August, the company announced plans to cut 15% of its workforce and suspend its dividend to reduce costs.

These measures, while painful, are seen as necessary to position the company for long-term success.

The most important area where Intel could see significant improvement is its foundry business.

Reports of a potential joint venture involving TSMC, Qualcomm, Nvidia, AMD, and Broadcom have sparked speculation about a strategic partnership that could revitalize Intel’s foundry operations.

Under the proposed deal, TSMC would take a minority stake in Intel’s foundry business, ensuring that the venture remains majority U.S.-owned.

This arrangement could help Intel access TSMC’s advanced manufacturing capabilities while addressing geopolitical concerns related to foreign ownership.

For TSMC, the partnership would further its goal of expanding its presence in the U.S., where it has already committed billions of dollars to build new fabrication plants.

The joint venture could also provide Intel with much-needed support in developing its 18A process node, which is set to enter mass production in mid-2025.

While Intel’s foundry business has struggled in the last few years, the company remains a dominant player in the PC market.

Despite losing market share to AMD in recent years, Intel still controls over 75% of the PC Client market.

The company is banking on its next-generation Panther Lake processor, built on the 18A node, to reignite growth in this segment.

Panther Lake, which is scheduled to launch in the second half of 2025, promises significant performance improvements and could drive a refresh cycle among enterprise customers.

Despite all these developments signaling a strong recovery, the market is still pessimistic about the company.

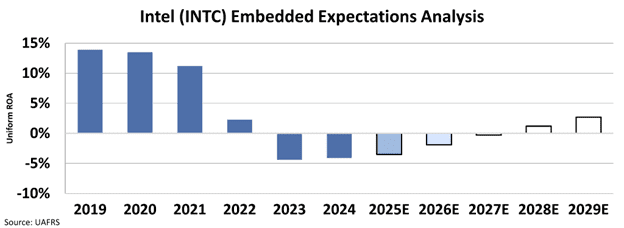

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s ROA will only improve to around 3%, far below historical levels.

Intel has strong tailwinds like potential tariffs forcing increased demand for the foundry business and the government supporting local chip manufacturing with the CHIPS act.

By focusing on innovation, streamlining operations, and exploring strategic partnerships, the company is positioning itself to reclaim its position as a leader in the semiconductor industry.

Trading at just 0.6x Uniform P/B, Intel presents a compelling opportunity for investors willing to bet on a potential turnaround story.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.