Shifting consumer preferences and rising global trade pressures are reshaping the competitive landscape for Nike (NKE). Industry leaders are being forced to rethink their strategies as younger rivals seize market share and economic headwinds weigh on demand. In today’s FA Alpha Daily, we explore how the world’s largest footwear company is navigating this transition and what it means for investors.

FA Alpha Daily

Powered by Valens Research

Nike (NKE) has dominated the global footwear market for decades, delivering impressive returns for shareholders as it continued to solidify and hold onto its dominant position.

However, the company’s performance has dragged over the past few years due to a combination of strategic missteps, competitive pressures, changing consumer preferences, and macroeconomic headwinds.

In the late 2010s, Nike transformed itself from selling products through department stores and wholesalers to selling directly to consumers. By 2021, this direct-to-consumer pivot eliminated 50% of its wholesale partnerships.

While the pivot boosted margins and enabled Nike to gather customer insights, it opened the door for rivals like Adidas, Skechers, and upstarts On and Hoka to flood wholesalers with their own offerings and capture market share.

Even though Nike still leads the global sports footwear market with 26% share as of 2024, this strategic misstep cost the company significant ground. After traffic stalled in both its physical stores and websites due to shifting consumer tastes, Nike announced it would repair its relationships with wholesale partners.

Rising prices due to inflation have likewise forced consumers to cut back on spending. Moreover, tariffs imposed on countries like Vietnam and China—where Nike’s factories are located—have further eroded the company’s prospects.

These challenges and results tanked investor sentiment, prompting a leadership change last year. John Donahoe retired and longtime company stalwart Elliott Hill took over as CEO.

As of September 30, Nike shares were down nearly 8% year-to-date. However, this reversed as shares rose 4% in after-hours trading following the release of first quarter fiscal 2026 results.

In a surprising twist, Nike beat expectations. The shoemaker posted quarterly revenue of $11.7 billion, a 1% year-over-year increase that surpassed consensus estimates of $11 billion.

Wholesale revenue jumped 7% to $6.8 billion while North American sales rose 4% to $5.02 billion, beating analyst estimates of $4.55 billion.

Against the backdrop of these positive results, Nike’s leadership cautioned that other segments may take longer to recover.

China sales fell 9% during the quarter, and the company likewise expects reciprocal tariffs to hurt its progress as tariff costs are projected to soar to $1.5 billion, up 50% from the initial $1 billion forecast for fiscal year 2026.

Overall, these results suggest that Nike’s turnaround strategy is finally gaining traction—a positive development for the market especially after years of declining returns.

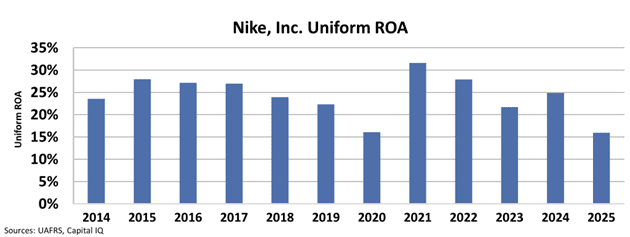

After generating a Uniform return on assets (“ROA”) of nearly 32% in 2021, Nike’s ROA has followed a downward trend, dropping slightly to 28% in 2022 and falling to just 16% this year.

The market is eager for Nike’s resurgence and return to historical levels of performance. Consequently, strategic moves and results that validate these expectations will be viewed favorably by the market.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.