International tourism was among the most severely affected sectors when the COVID-19 pandemic hit in 2020.

With borders closed and the whole world on lockdown, tourist arrivals fell by as much as 72%, going from 1.4 billion in 2019 to just 409 million in 2020—a trend that continued well into 2021.

By 2022, tourist arrivals steadily climbed as the world gradually reopened as nearly a billion tourists traveled across the globe. Fast forward to 2025, international tourist arrivals reached 1.5 billion, exceeding pre-pandemic levels.

With global travel surging, spending went up as well. According to UN Tourism data, export revenues from tourism—which includes receipts and passenger transport—reached $2.2 trillion last year. It’s also projected that 2026 will continue to be a strong year for international tourism, despite global uncertainty and geopolitical risks.

As a result of these positive trends, airlines, hotels, online travel services, and other companies deeply tied to the tourism sector saw tailwinds that enabled both recovery and growth.

And among these companies is Booking Holdings (BKNG).

Booking Holdings is the parent company of several online travel agencies, fare aggregators, and metasearch engines such as Booking, Priceline, Agoda, Kayak, Opentable, and others.

The company was founded in 1996 and went public three years after. At present, it is a leader in the global online travel market which is worth over $640 billion as of 2024. The firm operates in over 220 countries across the world.

Booking Holdings generates revenues through commissions from customer bookings across its vast brand portfolio. The company essentially operates as a platform, making it an asset-light business.

Booking, the company’s flagship brand, enables users to book property accommodations, flights, hotel rooms, rent cars, book attractions, and hire airport taxis in advance. It has 32 million reported listings as of September last year.

Meanwhile, as of the same period last year, over 1 billion room nights, roughly 64 million flight tickets, 87 million rental cars, and 621 million dining establishments were booked through Booking Holdings’ brands.

Booking Holdings has benefitted significantly from surging travel demand over the past few years and this has enabled it to grow its revenues significantly.

The firm grew its revenues from $6.7 billion in 2020 to almost $24 billion in 2024. Its returns follow a similar trend as well.

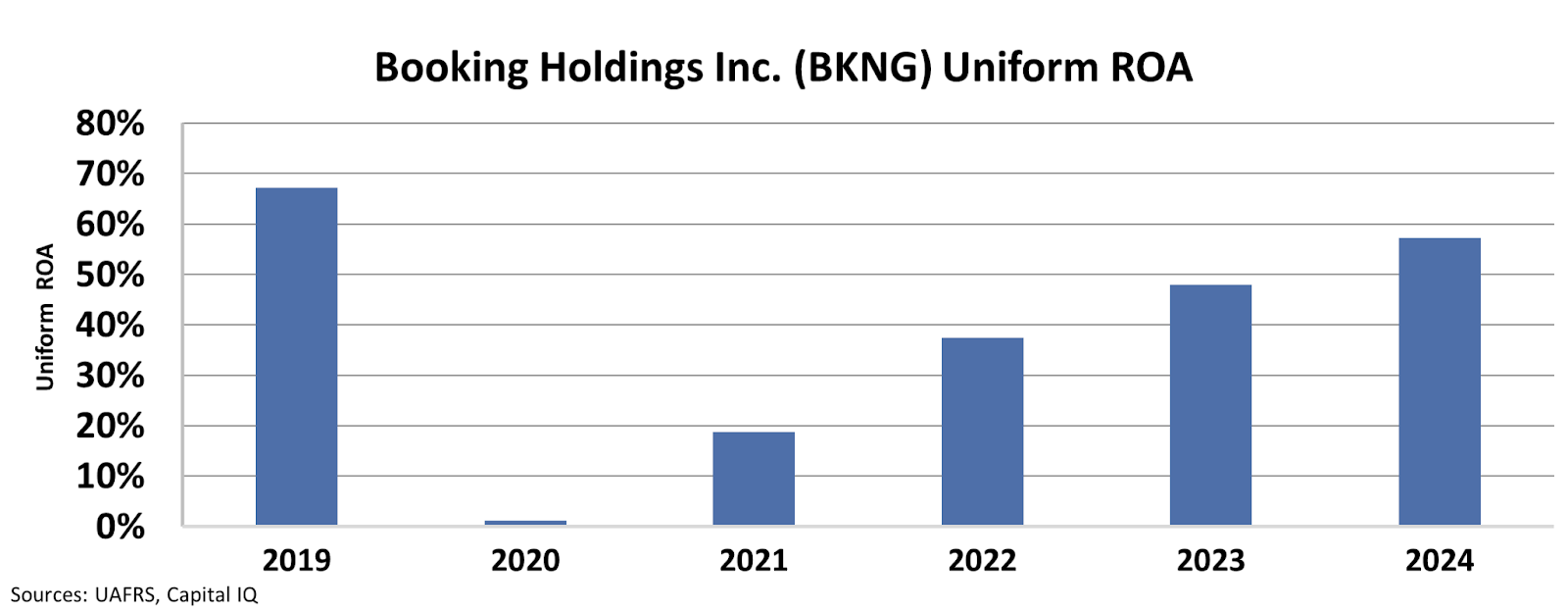

Booking Holdings delivered a Uniform return on assets (“ROA”) of 57% in 2024, a massive boost from the 1% returns it generated in 2020.

The company also delivered a Uniform asset growth of 9% in 2024.

Booking Holdings currently trades at a Uniform P/E of 35x. Despite this, the company’s current P/E ratio doesn’t fully reflect the durability of its margins, pricing power, and ability to deliver long-term growth.

With global travel demand and digital bookings expected to grow further, Booking Holdings is positioned for continued value creation and potential equity upside.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.