It’s common to hear that online shopping is destroying brick-and-mortar stores and that physical retail is on the decline. However, the situation is more complex than that.

While online shopping is certainly growing, physical stores still make up the vast majority of sales, over 83% in the United States.

The real change isn’t a battle between online and in-person, but a merger of the two. Today, most shopping trips start with online research.

While inside a store, 72% of people use their phones to look up reviews or compare prices. Smart retailers have even found that opening a new physical store can increase their online sales, a trend called the “halo effect.”

This new environment challenges older retailers like Macy’s (M).

They don’t have to disappear, but they must adapt to a world where the line between a website and a physical store has been erased.

For investors, the question is how well these companies can manage in this blended new world.

Macy’s presents a more compelling opportunity for debt investors than for those focused on equity.

The concerns of equity investors are understandable; shifting consumer habits, the persistent decline of traditional shopping malls, and the relentless growth of online retail create a challenging environment for a legacy brick-and-mortar giant.

While e-commerce has not completely overtaken physical stores, its growth consistently outpaces that of traditional retail, and Macy’s has struggled to capture a dominant position in this new landscape.

This has understandably cast a shadow over the company’s long-term growth prospects.

However, the pessimism that has impacted the stock has unduly punished the company’s debt. Creditors have driven bond yields to over 7%, a level that suggests a significant risk of default.

The S&P’s rating of BB+, or non-investment grade, reinforces this view, implying an 11% probability that Macy’s could default within the next five years.

While the company is unlikely to reclaim its former dominance in the retail sector, this outlook is overly negative.

A closer look at Macy’s financial health reveals a solid foundation for meeting its obligations.

The company demonstrates strong and consistent cash flow generation, a critical factor for any creditor.

Based on its latest earnings, Macy’s produced an annual free cash flow of $400 million, a figure derived from $1.3 billion in cash from operations minus $900 million in capital expenditures.

This robust cash generation provides a substantial cushion to service its debt payments. The company’s corporate cash flow profile shows a disciplined approach to spending and a proven ability to convert operations into cash, providing a significant margin of safety for debtholders.

The most compelling aspect of the investment thesis for Macy’s debt lies in its vast and undervalued real estate portfolio. This is the ultimate backstop for creditors.

While the book value of the company’s real estate is recorded at a depreciated historical cost of $2.3 billion, its actual market value is far greater.

Market-based estimates, which consider redevelopment or sale-leaseback potential, place the value significantly higher, with a blended “super” estimate suggesting a worth of approximately $8 billion.

This hidden value is a powerful form of credit enhancement. In a worst-case scenario, the monetization of these real estate assets would be more than sufficient to cover the company’s entire debt load, providing a recovery prospect that is not reflected in the current high yields of its bonds.

Given its solid financial standing, we believe Macy’s deserves a more secure rating.

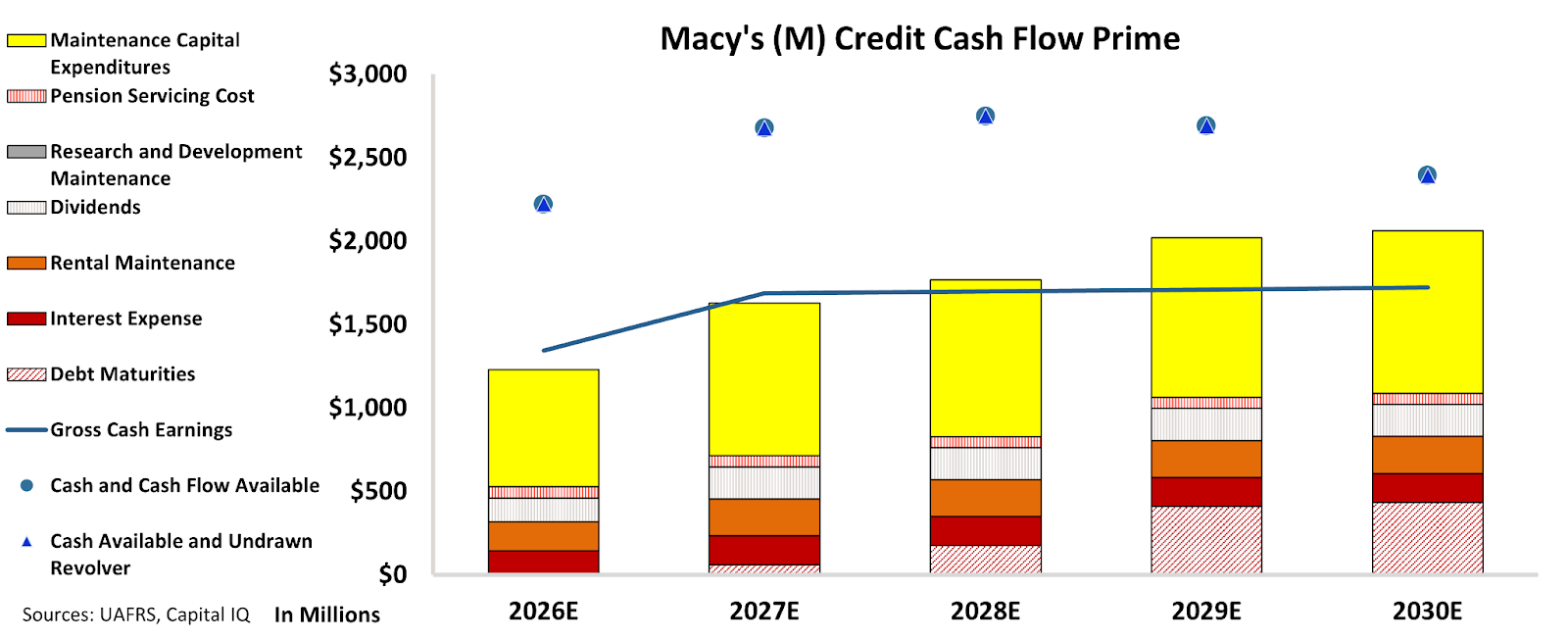

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Macy’s cash flows and cash available are more than enough to serve all its obligations going forward.

The chart indicates that the company is on solid financial ground and is likely to easily fulfill its obligations in the next five years.

The combination of steady, predictable cash flows and a hard asset base worth multiples of its recorded value means the risk of default is much lower than the market currently implies.

Furthermore, the firm’s robust 175% recovery rate on unsecured debt and sizable market capitalization should allow access to credit markets to refinance, if necessary.

Our review of Macy’s shows that the company has a low risk of default, contrary to what rating agencies indicate.

Therefore, we are assigning an “IG4+” rating to the company, which places it in the investment-grade basket, with a risk of default of about 2%.

The market is focusing on a weak growth story while ignoring a much stronger survival story, creating an opportunity for debt investors who prioritize steady income and capital preservation.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.