The pandemic has changed work life forever.

It has brought us the At Home Revolution, which makes us work, spend, live, and socialize from home.

With immense pace, we adapted to working remotely, using online tools to help us stay connected.

While management teams have made lots of noise about trying to bring people back into the office, that does not seem to be effective.

The fact is that some companies and employees are settling into an agreement about remote work.

Surveys show that workers want to spend roughly 2.3 days a week working in the office, and employers want them to spend 2.8.

Either way, no one is talking about putting the genie back in the bottle on remote work.

In fact, it is becoming permanent. Employees seem to like the chance to work from home with people close to them, usually at flexible hours.

Even though companies still try to promote coming to the office, they have already started using the remote option as a valuable recruiting tool.

Employees trying to run away from their 9-to-5 office jobs look for these opportunities and are specifically targeted by HR departments.

The biggest losers of this drastic change will, without a doubt, be office real estate investment trusts (“REITs”). They are going to see lower demand going forward, as companies need less office space.

A great example of these REITs is Douglas Emmett (DEI). The company owns a substantial share of top-tier office properties, premier multi-family communities, high-end executive housing, and key lifestyle amenities.

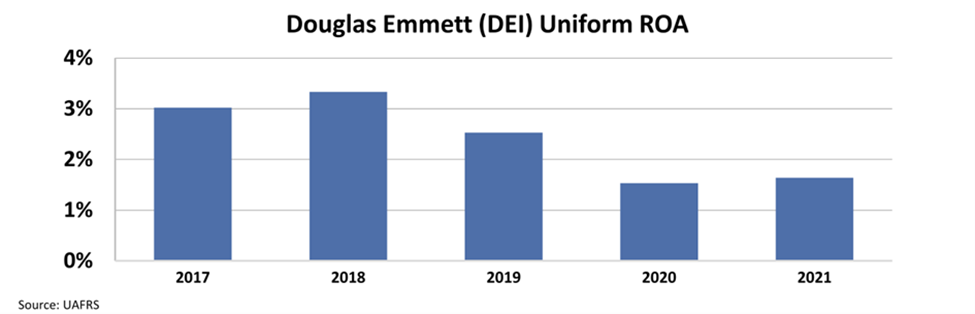

Impacted greatly by the pandemic, the company has seen its profitability go down very quickly.

The Uniform return on assets (“ROA”) has gone down from above 3% in 2018 to below 2% in 2021.

Even though this paints a pessimistic picture of the company, it does not imply much when it comes to investment decisions.

A company might still be considered cheap if the market expects it to perform even worse than what you expect. Therefore, we need to understand what the market thinks about Douglas Emmett.

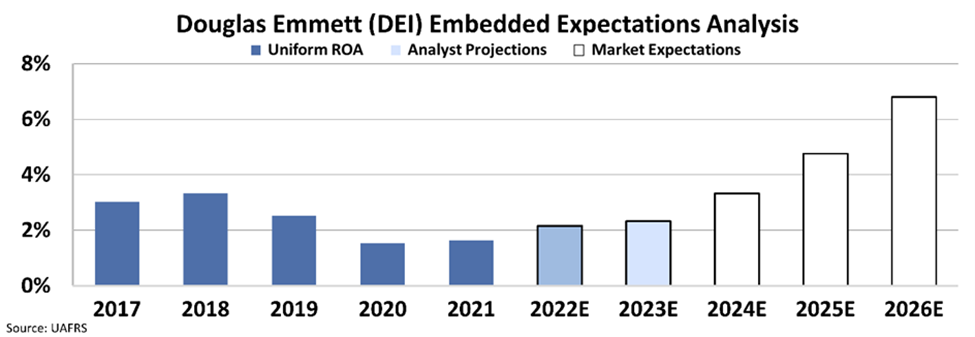

By utilizing our Embedded Expectations Analysis (“EEA”) framework, we can see what investors expect these companies to do at the current stock price.

Stock valuations are typically determined using a discounted cash flow (“DCF”) model, which makes assumptions about the future and produces the “intrinsic value” of the stock.

We know models with garbage-in assumptions based on distorted GAAP metrics only come out as garbage. Therefore, we use the current stock price with our Embedded Expectations Analysis to determine what returns the market expects.

At around $16, the market expects the company to have an unbelievable boost in profitability and reach almost 7% ROA in five years.

On the other hand, analysts are more pessimistic about the name and think it can only sustain an ROA of around 2%.

Considering the At Home Revolution and how working remotely is not going to disappear magically, the expectations seem incredibly high.

Douglas Emmett will probably not be able to reach those levels, and its investors are going to be disappointed.

That is why we have Douglas Emmett in our Thematic Short Idea List.

SUMMARY and Douglas Emmett, Inc. CorporationTearsheet

As the Uniform Accounting tearsheet for Douglas Emmett, Inc. (DEI:USA) highlights, the Uniform P/E trades at 71.6x, which is above the corporate average of 18.4x but below its historical P/E of 81.3x.

High P/Es require high EPS growth to sustain them. In the case of Douglas Emmett, the company has recently shown a 356% shrinkage in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Douglas Emmett’s Wall Street analyst-driven forecast is 1452% EPS growth in 2022 and a 30% shrinkage in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Douglas Emmett’s $16 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 34% annually over the next three years. What Wall Street analysts expect for Douglas Emmett’s earnings growth is above what the current stock market valuation requires in 2022 through 2023.

Furthermore, the company’s earning power is below its long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 270bps above the risk-free rate.

All in all, this signals high dividend risk.

Lastly, Douglas Emmett’s Uniform earnings growth is above its peer averages and in line with average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.