The AI boom has ushered in billions of dollars in spending on data centers. In 2026 alone, over $600 billion in spending commitments have been made by AI hyperscalers.

While this makes AI compute appear as the most valuable resource in the AI boom, the real bottleneck is power. Data centers consume gargantuan amounts of energy, with demand expected to reach nearly 76 gigawatts this year (“GW”) and further expand to 134 GW by 2030.

According to estimates, meeting this demand will require an investment of roughly $1.4 trillion in AI data center electrification.

Complicating this further is the current state of the U.S. power grid. This decades-old grid is already under pressure from surging electricity demand from households, manufacturers, utility providers, and recently, AI data centers.

To meet this challenge, America’s aging power grid will need to undergo modernization to replace aging equipment, materials, and components.

These glaring challenges have attracted the market’s attention, leading to a “picks and shovels” trade for two of North America’s largest infrastructure tailwinds today, positioning 138-year-old Hubbell Incorporated (HUBB) to benefit significantly.

Hubbell built its identity as a diversified manufacturer of electrical components, providing wiring, lighting, and utility hardware for both residential and commercial construction. Its founder, Harvey Hubbell II, invented the U.S. electrical plug and pull-chain light socket.

The company eventually evolved from a sleepy electrical hardware manufacturer into a high-margin specialist focusing on front-of-the-meter (“FTM“) and behind-the-meter (“BTM”) connectivity solutions.

FTM refers to storage and power generation systems like power plants, wind farms, and solar plants which are found before the meter. FTM systems provide power to electric grids and utility companies. On the other hand, BTM refers to the customer side of the utility matter. BTM systems include solar panels, battery storage, and backup power solutions.

Before the AI boom kicked into full swing, Hubbell’s growth was largely tied to steady and low-single-digit-cycles of building maintenance and grid upkeep for utility cooperatives. It generated revenue from a combination of hardware sales and equipment replacement.

Once the AI era rolled around, the company reinvented itself as a mission-critical power infrastructure provider, supplying end-to-end power solutions to modern data centers and offering a wide portfolio of products across data and communications, electrical, lighting control, and power and utilities categories.

Hubbell currently operates two major business segments, namely Hubbell Utility Solutions (“HUS”) and Hubbell Electrical Solutions (“HES”).

HUS is the company’s primary revenue generator. This segment specializes in grid infrastructure and grid automation. In the fourth quarter of 2025, this segment generated $936 million in revenue and is expected to grow further between 5% to 7% this year.

On the other hand, HES caters to data centers and the light industrial, non-residential, and heavy industrial markets. During the fourth quarter last year, this segment delivered $557 million in revenue and is forecasted to grow between 4% to 6% this year.

Despite Hubbell’s history and its pivot to a mission-critical electric infrastructure provider, investors relying on GAAP accounting have underestimated this business for many years.

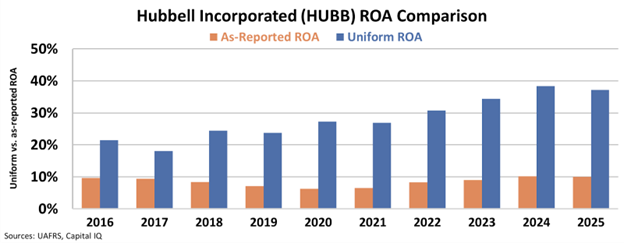

On the other hand, Seen through the lens of Uniform accounting, between 2016 and 2021, the company has consistently been more profitable compared to as-reported metrics.

And as the AI boom gained momentum, this disparity widened. In 2025, Hubbell’s Uniform return on assets (“ROA”) was 37%, significantly higher than the as-reported ROA of 10%.

Investors relying on as-reported metrics don’t understand just how profitable Hubbell is and how its profitability has grown in recent years.

As long as the market undervalues this firm, upside appears warranted for investors who can see just how crucial Hubbell is in the AI era.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.