The emergence and proliferation of electric vehicles (“EVs”) was a significant development in the automotive industry. As a result, EV stocks reached lofty valuations and expectations as the technology improved.

Over the past few years, EV technology has seen significant advancements, convincing carmakers and investors to pour billions of dollars into this technology in the hopes of benefitting from the transition from internal combustion engines to EVs and hybrids.

This trend was further boosted by favorable regulatory conditions. During the Biden administration, various clean-air, fuel economy, and EV-related subsidies were enacted and provided to incentivize the adoption of clean and low-carbon technologies.

Unfortunately, this proved to be a one-time tailwind. The Trump administration did away with many Biden-era EV adoption mandates and subsidies last year, pushing the EV industry towards a more volatile and uncertain phase.

In addition, demand has shrunk further due to economic pressures faced by consumers. Consumer credit stands at nearly $19 trillion dollars while inflation currently sits at 3.3%.

According to figures from Cox Automotive, nationwide EV sales fell to 216,000 during the first quarter of 2026, a 27% year-over-year decline. The sales dropoff was even worse during the fourth quarter of 2025, which saw a 36% decline.

In other words, EV sales are down, and that’s bad news for EV makers like Lucid Group (LCID).

Lucid Group, founded in 2007, started out as a manufacturer of EV batteries and power trains for car manufacturers. By 2016, the company announced its intent to manufacture long-range and high performance EVs.

Fast forward to February 2021, Lucid merged with Churchill Capital Corp IV, a publicly traded special purpose acquisition company (“SPAC”), paving the way for its public listing.

Since then, the company has positioned itself as a manufacturer of EVs for the luxury segment of the EV market.

Lucid’s current product stack includes four-door luxury sedan Lucid Air and SUV Lucid Gravity, released in 2021 and 2025, respectively.

Aside from developing models for consumer use, the company inked an agreement with Uber (UBER) last year that would see the latter integrate Lucid’s EVs to its ride-hailing network.

Unfortunately for Lucid, the EV industry is in the midst of a volatile phase. And this has been reflected in its most recent quarter.

During the first quarter of 2026, the company posted revenues of $282 million, a 20% year-over-year bump. However, this was far below the consensus estimates of $358 million.

Moreover, the company reported an operating loss of $989 million, far worse than Wall Street expectations of $864 million.

Management also announced the suspension of its production guidance for the year, citing the need for lowering its inventory of vehicles.

Lucid’s shares have fallen around 7% since releasing earnings on May 5.

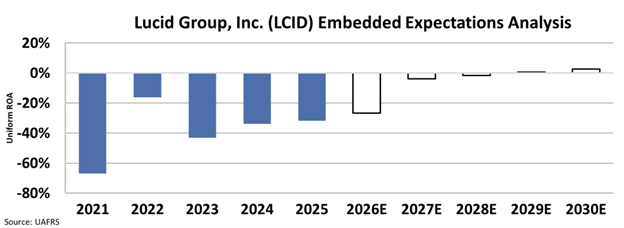

Since going public in 2021, Lucid has yet to generate positive returns. In 2025, the company’s Uniform return on assets (“ROA”) stood at -36.78%.

And moving forward, inventors expect returns to trend negatively.

This can be seen through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In other words, the EEA shows how well a company has to perform in the future to be worth what the market is paying for it today.

At current valuations, investors expect Lucid to keep posting negative returns until 2028. By 2029, Uniform ROA is forecasted to climb to 0.6% then 3% by 2030.

While these metrics indicate Lucid’s status as a cheap stock it is by no means undervalued.

Given that the company has continued to post negative returns since going public, the muted, if not downright negative, outlook is justified.

Investors currently expect the company to become profitable. However given recent results and current market headwinds, investors should not hold their breath.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.