After years of unprofitability and costly investments to build its streaming platform, Disney may finally be regaining its footing. With streaming losses narrowing, theme parks thriving, and revenue ticking higher, the entertainment giant is showing signs of a real turnaround. In today’s FA Alpha Daily, we explore how Disney’s turnaround could lead to a return to historical profitability and renewed investor confidence.

FA Alpha Daily

Powered by Valens Research

Disney (DIS) has faced years of weak performance and uncertainty as it dealt with pandemic-induced closures to its theme park business, resulting in billions in lost revenue.

These market headwinds came right as Disney was launching its own streaming platform, Disney+, to compete with Netflix, HBO, and Amazon in the latest media frontier.

The combination of park shutdowns and the costs of bringing its streaming platform to scale weighed heavily on Disney’s bottom line, driving its operating income down from $12 billion in 2019 to $3.5 billion in 2021.

Adding to the company’s volatility was the fact that long time CEO Bob Iger ceded control of Disney to Bob Chapek in early 2020.

Disney’s fortunes did not turn around during this time, as Disney+ generated operating losses exceeding $1 billion each year from 2020 to 2022. The company’s stock fell around 40% in this time, leading to the reinstatement of Iger in late 2022.

Since then, Iger has been able to right the ship, and Disney’s business has started to rebound. By the end of 2023 parks revenue had surpassed pre-pandemic levels and Disney+ had posted its first quarter of profits.

This trend continued in 2024, when Disney’s streaming division generated positive operating income for the year for its first time.

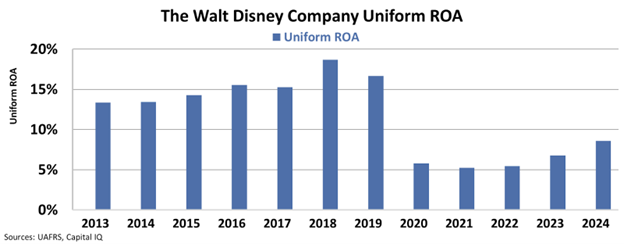

These improvements and Disney’s general recovery can be seen by looking at its Uniform return on assets (“ROA”).

Prior to 2020, Disney consistently generated returns greater than 10%. ROA fell to 5% in 2020 and remained compressed through 2022.

Since then, however, returns have increased thanks to the growth of Disney’s streaming platforms and the recovery of its experience businesses.

Last year Disney generated 9% ROA.

Disney has been trending in the right direction, and recent performance suggests this business could be on track to returning to past heights.

Revenue rose 2% year over year for the company, with its parks and experiences leading the way with 8% growth. Disney+ and Hulu added nearly 3 million new subscribers and the streaming segment as a whole posted record-quarterly profits of $346 million.

Disney also made waves with news of its acquisition of the NFL media rights. This deal gives Disney an advantage over its streaming competitors for the largest sport in the U.S.

Disney’s parks and experiences business has recovered from pandemic lulls. Its streaming platform has reached a scale where it is not only profitable but becoming more profitable as it grows. And now with its landmark NFL deal, the media giant’s sports division has a new catalyst for growth.

However, despite these positive trends recently, investors are still doubting this business. The market doesn’t believe that Disney will be able to replicate its past performances.

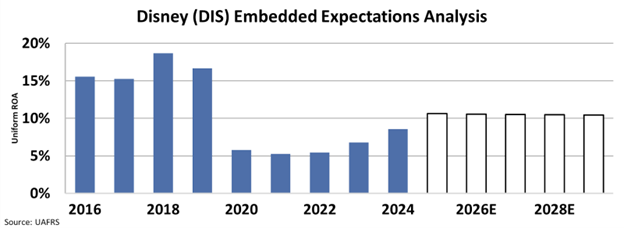

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

If Disney is able to continue its recent ascent off the back of continued improvements from streaming, and if the company’s new relationship with the NFL proves fruitful, Disney could see its ROA return to its former 15% levels. And when we consider the market’s current expectations, there is upside for this business if it can continue to execute.

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Investors understand that Disney’s worst days are behind it. This company has dealt with the growing pains of Disney+ and recovered from pandemic disruptions. That said, the market also believes that Disney’s best days are behind it.

While they expect Uniform ROA to improve this year, investors are forecasting Disney’s ROA to level out at 10% going forward.

Disney has proven that it can build out a profitable streaming platform. As this business continues to grow, and the company’s legacy divisions continue to perform, Disney’s returns could continue their ascent.

If this company is able to restore returns to historical levels, upside could be warranted for investors.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.