Boeing (BA), one of the world’s biggest aircraft manufacturers, has been in a slump in recent years due to production issues.

The aircraft manufacturer’s troubles began when its next-generation passenger aircraft, the 737 Max, was involved in multiple incidents and groundings from 2018, leading to regulatory scrutiny, penalties, and aircraft production caps.

As a result, Boeing’s aircraft deliveries plummeted from its 2018 peak of 806 to just 380 by 2019. Deliveries nosedived further to 157 planes in 2020 before recovering to 340 in 2021, 480 in 2022, 528 in 2023, and falling down to 348 in 2024.

Boeing made up for lackluster deliveries in 2024 by ramping up deliveries to 600 in 2025, helping it achieve better-than-expected results during the fourth quarter of that year.

Revenues surged to $23.9 billion, beating analyst estimates by $1 billion and representing a 57% year-over-year jump. Meanwhile, full-year 2025 revenues reached $89.5 billion, a 35% increase from the year prior.

Boeing’s leadership is banking on faster production to fuel the company’s continued recovery. And while this has signaled good tidings for the firm moving forward, this doesn’t mean it’s immune from hiccups.

Earlier this week, the company announced that it would delay the deliveries of some 737 Max planes due to scratched wiring in yet-to-be-delivered planes.

Though the company didn’t specify what repairs will be required or how many aircraft were affected, its company spokeswoman said that fixes could be completed in just a matter of days for each affected plane.

In response, the Federal Aviation Authority (FAA) said that it would look into the issue. Boeing’s shares fell roughly 3% after the announcement.

This recent hiccup could complicate Boeing’s attempts to convince regulators that it has effectively reduced manufacturing errors. However, the fact that the wiring issue was caught well before planes were delivered signals that the company has made some progress in its attempts to improve its quality assurance processes.

It remains to be seen whether this issue could slow overall deliveries. What’s clear is that Boeing intends to stick to its goal of delivering around 500 of its 737 Max planes this year—a notch higher than the 447 deliveries it made in 2025.

Setting this latest production issue aside, Boeing appears to be on the right track. Back in January, it was reported that it secured more orders than its rival AirBus (FRA:AIR) for the first time in a decade—receiving 1,075 in gross orders compared to AirBus’ 1,000.

Boeing’s stock is up 40% in the past year, and investors are expecting the company’s returns to return to its pre-2019 levels by 2030.

We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

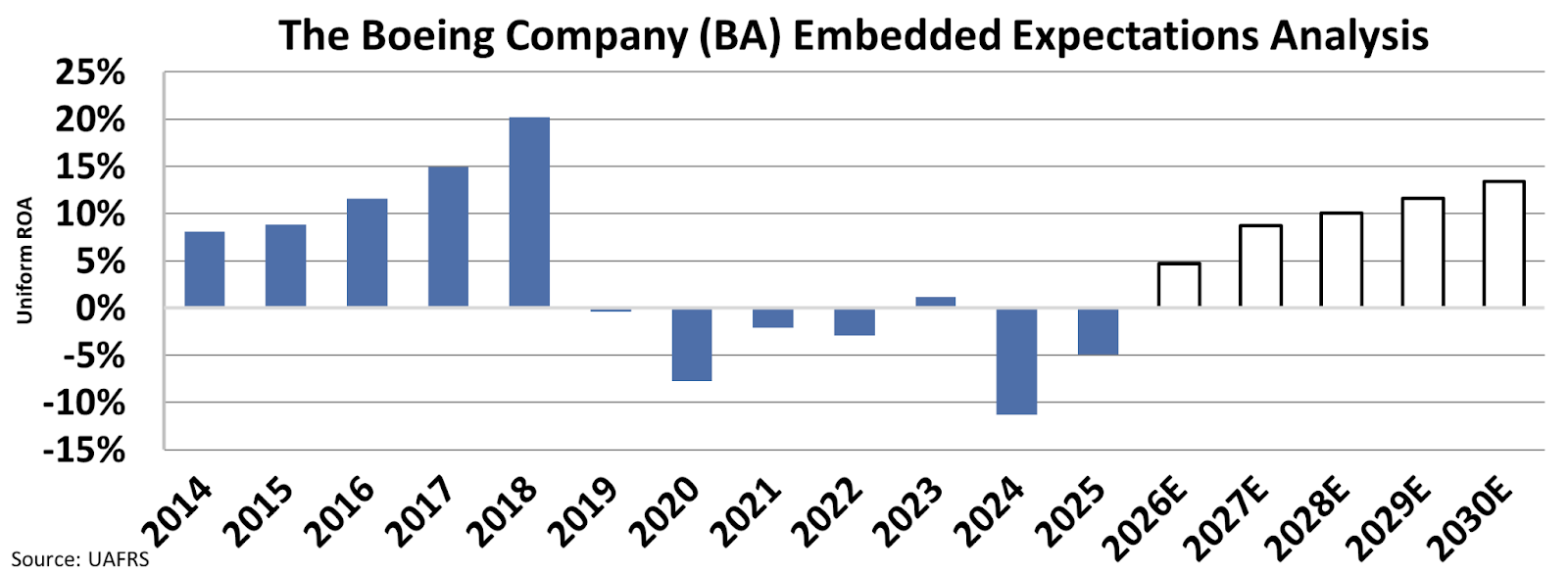

Prior to 2019—when Boeing started delivering negative returns—the company generated an average Uniform return on assets (“ROA”) of 13%.

Based on current valuations, investors expect the company to start generating positive returns this year, with returns climbing to 13% by 2030.

While it’s clear Boeing is making moves to improve its business, it’s too early to conclude that it has recovered. Thus, valuations and investor expectations appear to be too high for this embattled aircraft manufacturer to meet.

Boeing’s path to recovery will be a long and hard one, as it will have to prove that its manufacturing issues are behind it in the eyes of both regulators and customers.

Once that hurdle is cleared, only then could it be positioned to deliver positive returns and generate profits that are in line with investor expectations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.