In today’s interconnected world, technology typically advances concurrently across different regions.

This simultaneous development does not occur because each area independently discovers new innovations, but rather because the initial developers of new technology often license it to others globally.

A prime example of this is InterDigital (IDCC).

InterDigital has built a robust business model centered around licensing its intellectual property (IP) related to wireless communication and video technology.

The company is deeply embedded in critical technologies like Wi-Fi, 5G, and the forthcoming 6G, as well as advanced video compression solutions.

One of InterDigital’s major strengths is its extensive patent portfolio, which includes over 32,000 patents.

This allows the company to negotiate lucrative licensing agreements with major global smartphone original equipment manufacturers (OEMs), such as Samsung, Apple, and Xiaomi.

These agreements provide InterDigital with a steady stream of recurring revenue while positioning the company as a critical player in technologies that power over 70% of the global smartphone market.

The company recently secured deals with OPPO, Panasonic, and TPV, expanding its influence across smartphones, consumer electronics, and IoT devices.

InterDigital’s strength in video technology, especially its AI-driven video compression solutions, is a key growth driver.

These technologies enable high-quality streaming while reducing bandwidth requirements, which is a critical capability in today’s data-intensive environment.

This technology is valuable not only for smartphone OEMs but also for content providers like Netflix and Amazon, who are always looking for ways to improve streaming efficiency and reduce costs.

Beyond streaming, InterDigital’s AI technologies also enhance wireless network performance. This is increasingly important as the world transitions to 5G and eventually 6G.

The company’s AI-powered solutions optimize network efficiency, reduce latency, and improve the overall user experience, giving it a strong foothold in the evolving digital communication.

While smartphones remain a critical revenue stream, InterDigital is actively diversifying into the consumer electronics and IoT markets.

This segment showed an impressive 28% year-over-year growth in 2024. The IoT market is particularly exciting, with applications ranging from smart home devices and wearables to industrial automation and connected vehicles.

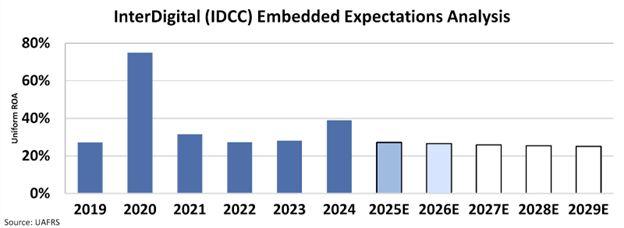

All these factors combined enabled the company to achieve 39% Uniform return on assets ”ROA” last year.

Despite this strong performance, the market has concerns about InterDigital’s reliance on licensing agreements.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to decline to 25%.

InterDigital’s reliance on licensing agreements means it must continually renew contracts with major clients.

The upcoming expiration of its agreement with Xiaomi is a potential concern. The Huawei contract’s end already impacted revenues.

However, InterDigital is executing well on its strategy to diversify its revenue streams while maintaining strong growth in its core markets.

Its leadership in both wireless connectivity and AI-driven video technologies offers a unique blend of opportunities that could drive long-term growth.

The company’s proactive approach to licensing and its expanding presence in consumer electronics and IoT markets are encouraging signs.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.