Every game in the casino is set up with the odds against you.

As the famous saying goes, the house always wins.

Winning in casinos is all about getting lucky and not sticking around long enough for the statistics to balance everything out in the casino’s favor, as it inevitably does.

One of the companies that helps casinos to make sure that people stick around longer is Everi Holdings (EVRI).

The company is a leading supplier of imaginative entertainment and trusted technology solutions for the casino and gaming industry.

It develops slot machine games and manages progressive jackpot gaming solutions for casinos that keep people playing with the hope of hitting the big jackpots.

Along with its strong presence in casinos, the company also provides server-based gaming solutions to digital gaming operators.

In addition, Everi Holdings is helping the casino and gaming industry with its financial technology products and services.

As the company provides essential services to the industry, it is no surprise that managing a business that prints cash means high profitability for the company.

Yet, S&P rates this cash flow generating machine as a B+, implying a 25% chance of defaulting.

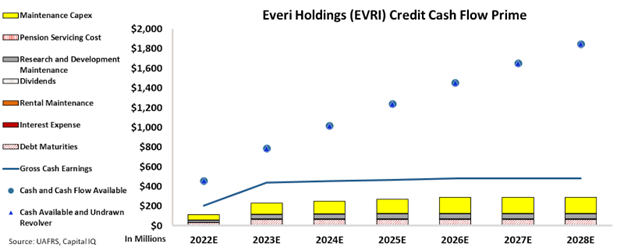

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (CCFP) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Everi Holdings’ cash exceeds all of the company’s obligations and its cash flows are consistently above its operating obligations for the next six years.

Looking at the CCFP chart, we can see that the company has almost three times more cash than its obligations and it also does not have any significant debt that would slow its operations.

This means that the company shows no risk of default for the next five years.

Also, considering the company’s leading position in providing essential services to the casino and gaming industry, a 25% chance of default makes no sense.

That is why Everi Holdings gets an IG3- rating from Valens, which corresponds to a default risk much less than what the rating agencies suggested.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Everi Holdings Inc. Tearsheet

As the Uniform Accounting tearsheet for Everi Holdings Inc. (EVRI:USA) highlights, the Uniform P/E trades at 10.8x, which is below the global corporate average of 18.9x and its historical P/E of 15.9x.

Low P/Es require low EPS growth to sustain them. In the case of Everi Holdings, the company has recently shown a 1005% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Everi Holdings’ Wall Street analyst-driven forecast is for a 26% and 2% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Everi Holdings’ $16 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2021 is 13x the long-run corporate average. However, cash flows and cash on hand are more than 3x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 530bps above the risk-free rate.

Overall, this signals a high credit risk.

Lastly, Everi Holdings’ Uniform earnings growth is above its peer averages and is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Everi Holdings Inc. (EVRI) credit outlook is the same type of analysis that powers our macro research detailed in the member-exclusive FA Alpha Pulse.