As the artificial intelligence (“AI”) revolution continues to accelerate demand for energy, companies, and highly-developed countries like the U.S., are looking for ways to meet rising energy demand.

The search for energy has likewise led to the revival of the nuclear industry and a further push towards renewables and other clean sources of energy.

Despite the exploration of those alternatives, the oil and gas industry remains to be the biggest supplier of energy, as oil is still forecast to remain as the world’s largest source of energy for the next two decades, supplying 30% of the world’s energy demand by 2035.

It’s estimated that the world will need to spend as much as $540 billion annually on oil and gas exploration to keep up with demand and maintain current output by 2050 as existing oil fields decline due in part to worldwide dependency on U.S. shale.

This forecast also means that companies will need to search for reserves that have yet to be discovered.

With oil and gas set to remain as the world’s primary sources of energy, companies that specialize in providing the technology and equipment needed for offshore exploration are well-positioned to capitalize.

TechnipFMC (FTI), an oil and gas equipment and services provider, is an example of a company that will likely benefit from the continued dependence on oil.

The company was formed in 2017 as a result of a merger between FMC Technologies and French oil services firm Technip SA.

The merger did not play out as had been hoped. After rising in each of the previous two years leading up to the merger, TechnipFMC’s operating income declined in 2018 from $1.3 billion to $950 million. Operating income fell again in 2019 to just $113 million.

In 2019, it was announced that the company would be spun off into two different entities. This spin-off was eventually completed in 2021, after being delayed due to the COVID-19 pandemic.

At present, TechnipFMC operates two core business units: Subsea and Surface Technologies. The former manufactures and delivers subsea equipment and controls and life of field services.

Surface Technologies, on the other hand, provides wellheads, surface trees, drilling pressure pumping, measurement equipment, production, and frac and flowback services globally.

In addition to those core segments, the firm also has an energy transition unit that caters to offshore floating renewables such as wind and tidal and is currently developing offerings for greenhouse gas removal, hydrogen generation, and even storage and electrification.

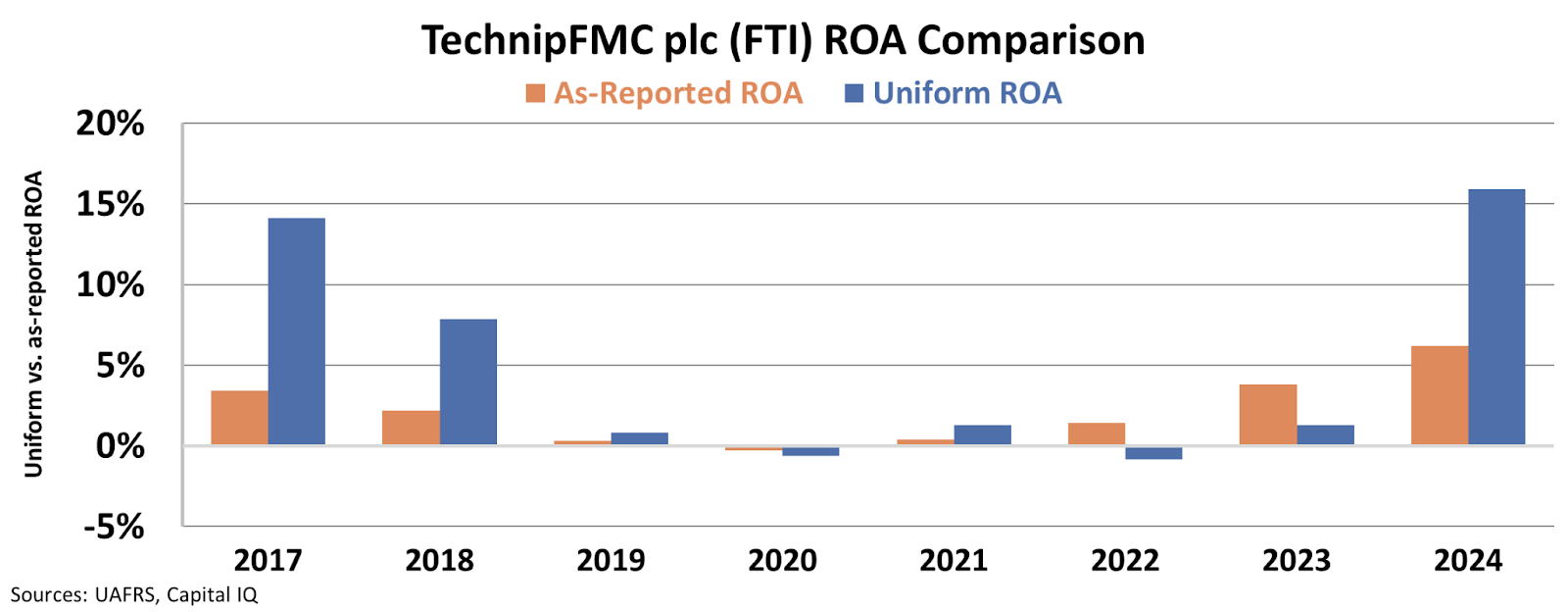

Since 2019, the company has struggled to generate returns amid spinoff delays and a difficult oil and gas environment in 2020.

However, since the spin-off in 2021, TechnipFMC has slowly rebounded as it focused its efforts on its core operations. As a result, its Uniform return on assets (“ROA”) has rebounded from 0.8% in 2019 to 16% last year.

While it’s clear from a Uniform Accounting perspective that the company has managed to fix its business, the market seems to be missing this turnaround.

Investors relying on as-reported accounting metrics only see an unprofitable company. Based on GAAP metrics, TechnipFMC generated a ROA 6% last year, well below the corporate average of 12%.

As Uniform accounting has shown, TechnipFMC is a more profitable business than investors realize. And if it can continue to improve its returns in this bull market environment and capitalize on continued reliance on petroleum, then upside could be warranted.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.