Software stocks have been under pressure as investors question how artificial intelligence will reshape traditional technology business models. At this point, markets are selling potential winners alongside companies truly at risk. In today’s FA Alpha Daily, we examine why ExlService (EXLS) could be one of the overlooked winners as AI adoption accelerates.

FA Alpha Daily

Powered by Valens Research

Software stocks have fallen to massive selloffs this year. Investors worry that large language models and new AI tools could pressure older software businesses. In some cases, that fear is justified.

The S&P Software & Services ETF (XSW) is down roughly 18% year-to-date.

However, the market may be painting with too broad a brush.

ExlService (EXLS) looks like one of the names caught in that selloff, even though it may actually be a winner from the AI shift.

EXL isn’t a typical software business. It operates much closer to an “asset-based” consulting model. The company builds proprietary software tools for insurers, healthcare companies, and banks. Then, it keeps consultants in place to run and refine those tools over time.

That structure makes the business far stickier than either standalone software or traditional consulting.

There’s no natural end date, customers keep paying EXL year after year to operate and optimize critical systems. With more than 800 clients and over three-quarters of revenue recurring, the model is built for stability.

And that stability is especially valuable now.

While many software companies are still debating how AI will affect their products, EXL has already built its strategy around it.

The company has transformed itself into a data-and-AI-led business. Revenue tied directly to data and AI has risen from 38% in 2020 to 53% in 2024. The company now employs more than 4,500 AI specialists. It has built 16 AI agents, 20 AI solutions, and seven domain-specific large language models.

AI isn’t disrupting EXL’s moat, it is strengthening it.

Uniform Accounting shows that strength clearly.

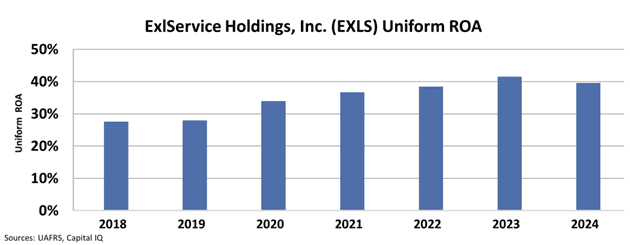

EXL’s Uniform return on assets (“ROA”) has climbed from an already impressive 28% in 2018 to 40% in 2024. The company is still growing to meet demand. Last year, EXL expanded its asset base by 14%.

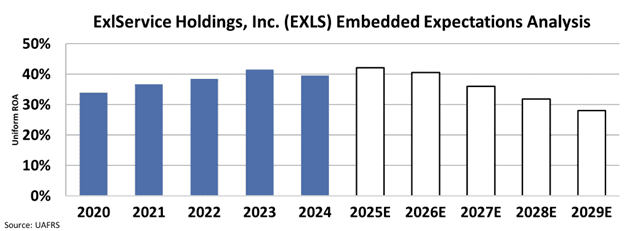

Yet despite that performance, the selloff has pushed EXL down to just 14x Uniform P/E—the lowest valuation the company has seen in more than a decade. At today’s levels, the market is pricing in a drop in Uniform ROA back to around 30% by 2029.

That is a cheap multiple for a business with sticky clients, recurring revenue, and a model reinforced—not threatened—by AI adoption.

The market seems to be treating EXL like every other software business facing AI disruption. But EXL looks more like the opposite. It’s a company with a durable moat that may actually benefit as companies lean more heavily into data-driven and AI-enabled operations.

If software and AI names recover, the company could be one of the clearest beneficiaries. Its economic model, client base, profitability profile, and valuation all point to a company that has been misclassified in a broad selloff.

For investors willing to look beneath the surface, EXL offers the combination the market rarely gives: recurring revenue, rising returns, strong AI positioning, and a decade-low valuation.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.