Companies with durable competitive advantages tend to generate higher returns and sustain outperformance over time. However, not all moats are equal, and the market often assumes these advantages will fade, leading to mispriced opportunities. In today’s FA Alpha Daily, we examine why certain types of moats are more durable than expected and how investors can identify businesses positioned to outperform.

FA Alpha Daily

Powered by Valens Research

See’s Candies is a paradise for chocolate lovers of all ages.

This West Coast staple is beloved for its high quality ingredients and wide selection of flavors. Patrons who visit are also greeted by friendly staff and welcomed with free samples.

However, customer service and high quality products aren’t the reasons why Warren Buffett invested in the company.

Buffett invested in See’s Candies decades ago because he saw an above-average company. In a 1983 investor letter to Berkshire Hathaway shareholders, he highlighted that the company was earning a return on assets (“ROA”) of 25%, more than double the 11% corporate average.

The secret lies in the See’s Candies brand. This cult-classic chocolate maker has been winning over customers since the 1920s.

Patrons love the nostalgia of walking into a See’s store and customizing their own box. They’re excited to pick up a few pieces of their childhood-favorite chocolates. They’re thrilled to see their loved ones’ faces light up at the iconic checkerboard packaging.

And they’re happy to pay a few extra dollars for the See’s experience over a cheap drugstore option.

This advantage leads to what Buffett calls economic goodwill. It’s a fancy way of saying folks have no problem spending more on the chocolates than it actually costs to make them.

That’s why See’s Candies’ revenue rose by $46 million from 1979 to 1983 while profits doubled from $6.3 million to $13.7 million even as production stayed pretty much flat.

Buffett talked more about economic goodwill in future letters. Eventually, he expanded to a number of other key competitive advantages (he called them “moats”). Each can give a company a unique leg up on the competition.

Companies with competitive advantages tend to outperform peers without any and they tend to be rewarded by the market.

The right moat can create a lasting edge, making a business nearly impossible to dethrone.

That said, not all advantages are created equal. In the course of our research, we’ve identified 14 main types of competitive advantages.

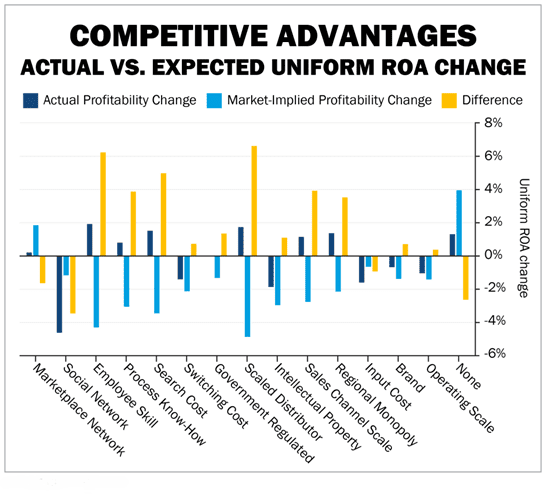

In almost all cases, the market expects profitability to return to average levels in the long run as a company’s advantage over the industry fades over time.

The market tends to underestimate most advantages. When the yellow bar is positive in the chart below, that means that type of competitive advantage is stronger than the market realizes.

Companies with advantages that are stronger than the rest of the market realizes tend to outperform expectations. For example, businesses with the “scaled distributor” advantage can add about 2 percentage points to profitability while the market expects them to lose more than 4 percentage points.

As businesses with stronger-than-expected advantages get even stronger, the market will be forced to reward those stocks eventually.

And investors who spot those winners early on are the ones best positioned to realize outsized gains.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.