I was recently asked at a conference about a credit opportunity that I thought was interesting, and the first bond that came to mind was Laredo Petroleum.

It is an independent energy company, which engages in the acquisition, exploration, and production of oil and natural gas in the Permian Basin of West Texas.

No one thinks that it’s compelling due to the cyclicality of the business and people are always worried about what happened to it in 2015, instead of looking at the reality.

One of the most important drivers of profitability in the oil and gas industry, especially for the companies engaged in exploration and production, are commodity prices like crude oil.

As West Texas Intermediate (WTI) crude oil prices started to fall from around $100 per barrel in the first half of 2014 to around $35 by the end of 2015, many oil and gas companies suffered through this period and Laredo Petroleum was one of them.

An immense 65% fall in crude oil prices affected these companies significantly.

However, for credit investors, the single most important thing is a company’s ability to pay its obligations, and Laredo had no problems with it.

Yet, it seems like credit rating agencies are still worrying about the cyclical and volatile nature of the business and are rating it with a high chance of default.

S&P gave a B rating for the company, implying a 25% chance of default.

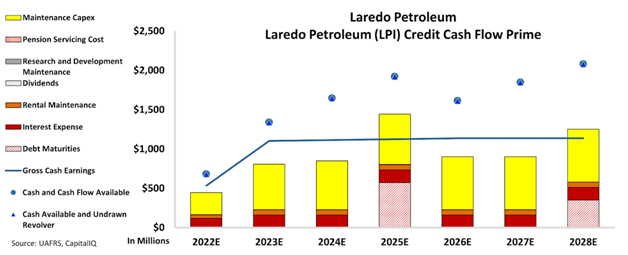

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Laredo’s cash flows are much more than enough to cover its operating obligations and the company has a remarkable cash buffer to cover its financial obligations as well.

As the CCFP chart shows, Laredo’s cash flows should be plenty to cover its operating obligations through 2028.

Also, in the two years with debt maturities, 2025 and 2028, cash flows alone won’t totally cover operating obligations and debt maturities. However, when factoring in its cash buffer, the company has no problems paying all its obligations.

Laredo also specifically announced that it has a debt repayment target totaling $700 million by the year-end of 2023.

This shows that the company can manage its obligations effectively, even as its bonds are yielding around 10%.

That’s why giving it a rating with a 25% chance of default does not seem very realistic.

Instead, we think it should have much less credit risk and give an “XO” rating to the company, meaning that it can navigate its issues, with a lot less risk of default than 25%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Laredo Petroleum Tearsheet

As the Uniform Accounting tearsheet for Laredo Petroleum (LPI:USA) highlights, the Uniform P/E trades at 10.5x, which is below the global corporate average of 17.8x and its historical P/E of 51.9x.

Low P/Es require low EPS growth to sustain them. In the case of Laredo, the company has recently shown a 18% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Laredo’s Wall Street analyst-driven forecast is for a -260% and 92% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Laredo’s $67 stock price. These are often referred to as market embedded expectations.

However, the company’s earning power in 2021 was below the long-run corporate average. Moreover, cash flows and cash on hand were below its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 480bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, Laredo’s Uniform earnings growth is below its peer averages and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Laredo Petroleum (LPI) credit outlook is the same type of analysis that powers our macro research detailed in the member-exclusive FA Alpha Pulse.