Pharma companies are cash flow machines once they manage to get approvals and release a few drugs to the market.

Of course they have to be concerned about patent cliffs and approvals for their branded drugs, as any disruption could hurt cash flows. But it does not mean that they’d again be in the wilderness without cash flow.

In fact, once they start to make money, it’s really hard for them to start losing money.

This is especially true if the company is a good innovator and finds new treatments, and also if they can manage to maintain stability by selling popular generic drugs.

That’s exactly where ANI Pharmaceuticals (ANIP) positions itself, as an innovative and stable cash flow machine.

The company has been steadily generating a return on assets (ROA) of above 15% during the last decade.

Wall Street analysts’ forecasts show that the company will continue to do so over the next few years.

However, S&P is imagining ANI is still a start-up. It rates the company with an overstated risk of default.

S&P thinks there’s a 25% chance that ANI Pharmaceuticals goes bankrupt in the next 5 years as it gives ANI a B+ rating.

A quick look at its stable returns and fundamentals shows that make no sense at all.

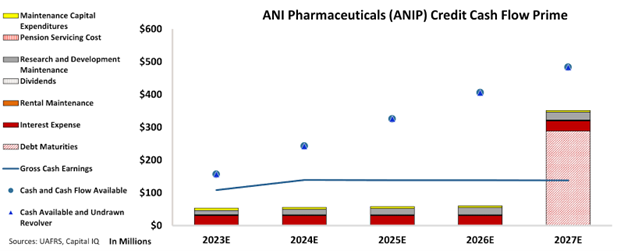

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart clearly shows that ANI Pharmaceuticals’ cash flows are more than enough to cover its obligations going forward.

The chart shows ANI does not have any concerning debt maturities or obligations until 2027.

And even if the company doesn’t refinance the 2027 debt headwall before it comes due, thanks to its massive cash flow generation relative to obligations, cash on hand should be more than enough to handle the company’s debt maturity.

Considering these factors, we don’t see a significant credit risk for the company, and we think that it should be much safer than what credit rating agencies think.

Hence, we are giving an “IG3+” rating to the company, which implies around a 1% chance of default as opposed to S&P’s overstated 25% risk of collapse.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and ANI Pharmaceuticals (ANIP:USA) Tearsheet

As the Uniform Accounting tearsheet for ANI Pharmaceuticals (ANIP:USA) highlights, the Uniform P/E trades at 10.1x, which is below the global corporate average of 18.4x and its historical P/E of 11.4x.

Low P/Es require low EPS growth to sustain them. In the case of ANI Pharmaceuticals, the company has recently shown a 9% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ANI Pharmaceuticals’ Wall Street analyst-driven forecast is for a 53% and 33% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ANI Pharmaceuticals’ $38 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2022 was 3x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 860bps above the risk-free rate.

Overall, this signals a high credit risk.

Lastly, ANI Pharmaceuticals’ Uniform earnings growth is in line with its peer averages and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of ANI Pharmaceuticals’ (ANIP) credit outlook is the same type of analysis that powers our macro research detailed in the member-exclusive FA Alpha Pulse.