Editor’s note: We’re interrupting our regularly-scheduled FA Alpha 50 so we can talk about one of the trendier names in the consumer products space.

Brand loyalty can transform everyday products into highly profitable businesses with enduring customer appeal. However, maintaining that success can become increasingly difficult as competition intensifies and consumer preferences evolve. In today’s FA Alpha Daily, we examine why the market remains cautious on YETI Holdings (YETI) despite its strong operating performance.

FA Alpha Daily:

Stock Analysis

Powered by Valens Research

The value of consumer products often surpass the utility of a good and extend to the status symbol one achieves by owning a certain brand.

For decades this has been true for big-ticket things like cars, phones, appliances, and designer fashion brands.

But in recent years a brand battle has taken place in the historically mundane reusable water bottle market.

Over the past 10 years this market has grown from around $7 billion to nearly $12 billion today. One of the largest companies in this space today is YETI Holdings (YETI).

57% of the company’s sales come from drinkware like stainless steel tumblers and water bottles. Another 41% is derived from coolers and outdoor equipment, while a small percentage of revenue comes from apparel and accessories for its main segments.

The company’s products are known for their durability. YETI coolers can keep ice frozen for two to five days, and its tumblers keep drinks cold for more than 24 hours.

These extremely durable products have garnered a cult-like following from consumers over the past decade. This has helped the company’s revenue grow from $639 million in 2017 to $1.9 billion over the past twelve months.

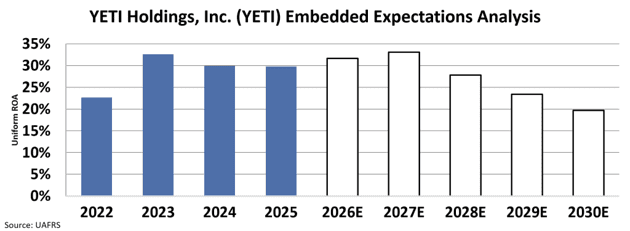

Meanwhile, YETI’s Uniform return on assets (“ROA”) has expanded from 19% to 30%.

However, like many consumer products YETI competes in an industry full of replicants and competitors offering similar products. In the world of reusable water bottles, fads dictate which brands are popular, and changing preferences limit YETI’s growth prospects.

In recent years brands like Hydro Flask, Stanley, and Owala have all emerged and taken market share from YETI.

Last year Stanley, a private brand, generated an estimated $750 million and $800 million in sales, within touching distance of YETI’s $1.09 billion in drinkware sales.

Given mounting pressure from competing brands, investors have tempered their expectations for the outdoor goods brand.

Despite strong returns in recent years, YETI trades at a below-average P/E of 15x, signaling that the market is cautious about consumer spending and competitive pressures. At this valuation, the market expects the company’s ROA to deteriorate to 20% by 2030, its lowest level in more than five years.

YETI has been an industry leader of the reusable water bottle and outdoor cooler market for years. However, like many consumer products, low barriers to entry and often-changing consumer products make it difficult for a brand to withstand the fate that many fads eventually face.

Investors expect YETI’s profitability to compress in the coming years as pressure from competitors mounts.

The market is correct to take this stance. This business trades at a discount for a reason. It is best to stay away.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis only scratches the surface of what we share with our FA Alpha Members. If you want to gain an in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.