Last week we talked about one of the areas growing and innovating immensely.These are healthcare companies, and in particular, the ones working in synthetic biology.

The combination of engineering and biology solves many problems in various areas from medicine to agriculture.

While we focused on the companies that enabled this surge in research and innovation by providing equipment last week, today we will see how this growth helps a different business.

Life sciences companies might be under the spotlight for doing the actual research and development. Yet, they operate in a “winner take all” market.

The first one to discover the product gets most of the credit and enjoys high profitability for years to come.

However, there is one company that will benefit from the surge in innovation regardless of who wins it. And it is clear that we are not the only people who recognize it.

Elliott Capital is acquiring a player that helps support innovation in healthcare, Syneos Health (SYNH), for $43 a share.

The company is everywhere from the initialization of a life sciences project to the commercialization of it.

With its clinical solutions segment, Syneos helps with clinical development and provides regulatory consulting, project management, and monitoring.

In the meantime, its commercial solutions segment is responsible for public relations, advertising, and medical communication.

Elliott Capital sees the continued boom of innovation and knows how Syneos is going to be an essential part of it.

Interestingly though, it seems like they got the company for a steal…

$43 per share means they are paying a 24% premium on Syneos’ share price before the announcement. This is lower than the healthcare sector average.

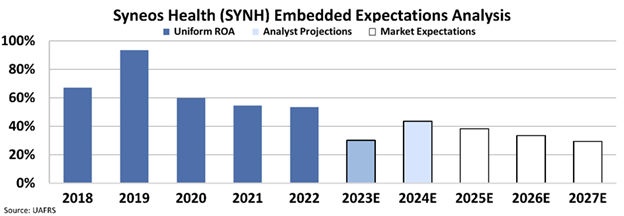

More importantly, we can see how well Syneos Health has to perform in order to justify a $43 per share price tag through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

Over the last five years, Syneos enjoyed a return on assets (“ROA”) of around 60%. In fact, it was immensely profitable in 2019, with ROA reaching 93%.

At $43 per share, the company only has to have an ROA of above 29% to justify its valuation.

For a company that is and will be at the center of healthcare innovation, thinking that the business will be less profitable going forward seems pessimistic.

If ROA is likely to accelerate again because of booming innovation after the post-COVID chill, the company would be worth even more than what Elliott pays.

And that means lots of potential upside…

SUMMARY and Syneos Health, Inc. Tearsheet

As the Uniform Accounting tearsheet for Syneos Health, Inc. (SYNH:USA) highlights, the Uniform P/E trades at 20.3x, which is around the corporate average of 18.4x and its historical P/E of 19.3x.

Average P/Es only require average EPS growth to sustain them. In the case Syneos Health, the company has recently shown a 11% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Syneos Health’s Wall Street analyst-driven forecast is a 52% EPS shrinkage in 2023 and a 64% EPS growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Syneos Health’s $41.54 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 10% annually over the next three years. What Wall Street analysts expect for Syneos Health’s earnings growth is below what the current stock market valuation requires in 2023 but above its 2024 requirement.

Furthermore, the company’s earning power is 9x its long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 380bps above the risk-free rate.

All in all, this signals average credit risk with no dividends.

Lastly, Syneos Health’s Uniform earnings growth is below its peer averages but in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.