Rising geopolitical tensions are pushing oil prices higher and fueling concerns about global economic stability. However, past market reactions suggest these events often lead to short-term volatility rather than lasting damage. In today’s FA Alpha Daily, we examine why current oil price levels may not signal a deeper crisis and what actually drives markets.

FA Alpha Daily

Powered by Valens Research

Investors have had plenty of reasons to panic in the past month.

The U.S. strike on Iran was enough to drum up a fresh batch of uncertainty. Stocks fell nearly 8% in March and investors don’t seem too sure about what the market holds for the future.

Investors previously expected two more rate cuts this year. Now, they expect none.

Likewise, with transit in the Strait of Hormuz well below pre-war levels, oil prices are on the rise. Brent crude (the international standard) has hovered around $100 or more per barrel throughout the conflict, up from roughly $60 in mid-February.

Brent crude prices, at least for now, have fallen below $100 after a two-week ceasefire was announced on April 8.

Investors are cautiously optimistic so far. The conflict could pick up again, driving oil prices up once more. Investors are preparing for the worst.

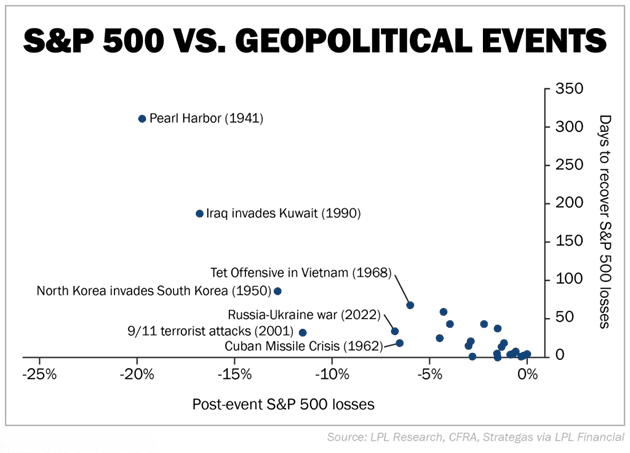

But history reveals that’s probably not necessary. While markets typically wobble on geopolitical shocks, they rarely break. The chart below shows how stocks have reacted to more than two dozen major geopolitical events since World War II.

The S&P 500 Index’s average decline during these events is about 4.5%. Markets typically bottom in roughly 18 days and recover fully in less than 39 days.

Put simply, these events tend to create more fear than lasting fundamental damage. The typical pullback has been shallow. And the recovery tends to arrive faster than investors expect.

That’s especially true when we look at geopolitical events that occurred nowhere near a recession, such as when the Israel-Hamas war which started in October 2023.

Following events that happen near a recession, the S&P has averaged negative returns within one, three, six, and 12 months.

In non-recessionary backdrops, returns have been positive for all of those time spans.

The market can absorb geopolitical volatility. It struggles when that volatility arrives at an already-weak time.

The key question for investors right now isn’t if the Iran conflict is serious. It is.

From a market perspective, the more important question is whether or not the conflict is going to push the U.S. into a recession.

Without a doubt, high oil prices are the fastest way to plunge the global economy into recession.

The Strait of Hormuz carries roughly 20% of the world’s oil supply. And prolonged disruption is the clearest risk that could keep prices high for the foreseeable future.

That hasn’t happened yet. In the past, it has taken sustained prices above $120 per barrel to drive a recession.

Kristina Hooper, chief market strategist of investment-management company Man Group, thinks that’s the lowest point at which investors should worry. She believes it would take sustained prices between $120 and $130 per barrel to drive a recession in the U.S.

Vanguard thinks the price is even higher. It predicts that oil prices would need to remain above $150 per barrel for the rest of the year to drive the country into a recession.

These estimates show what a strong base the U.S. economy has built.

The market backdrop remains constructive as long as credit stays supportive and earnings growth keeps carrying the load.

Neither of those factors has changed. So unless another factor does—like much higher oil prices for a sustained period—there’s no reason the economic story should change, either.

Investors should keep an eye on oil and not the headlines. If the commodity normalizes, this episode will probably go down as another reminder that geopolitical fear doesn’t always doom the market.

And unless recession risk spikes, this kind of sell-off is more likely a buying opportunity than the start of a lasting bear market.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.