Undoubtedly, Tesla (TSLA) has successfully reigned over the electric car industry in the last few years as the first mainstream electric car manufacturer. However, credit rating agencies still gave the company a BB+ rating, despite the incredible amount of cash backing its operations. Today’s FA Alpha Daily will investigate the company’s real creditworthiness.

FA Alpha Daily:

Wednesday Credit

Powered by Valens Research

Elon Musk has been unable to avoid the headlines for the last few years.

Thanks to his online presence and willingness to express his opinion on pop culture, cryptocurrencies, and policy, he has been a magnet for news.

Whether the Twitter debacle, his attempt to rescue stranded kids in Thailand, or his confrontational attitude towards shareholders and governments, there are plenty of topics to choose from.

People on the internet called him a speculator, a fraud, and a lunatic, but he never stopped doing what he does best.

One thing that no one can fault him for though is how successful at building businesses he is. While working on getting people on Mars with SpaceX, he managed to build Tesla (TSLA) into the giant of the electric vehicle (EV) industry it is now.

The brand is so huge that it is the first image that comes to mind for many when thinking about electric vehicles.

At a market cap above $700 billion, a revenue of $62 billion, and a free cash flow of $6.4 billion in the last twelve months, Tesla has been flourishing as the first mainstream electric car company.

However, there is one set of critics that still has not caught on to how successful he has built the firm to be: the credit agencies…

Rating the company at BB+, they are saying that there is a 10% chance that Tesla is at risk of default.

Seeing that the company has $18 billion in cash and only $3.4 billion in debt, it is laughable how much these agencies are missing the picture.

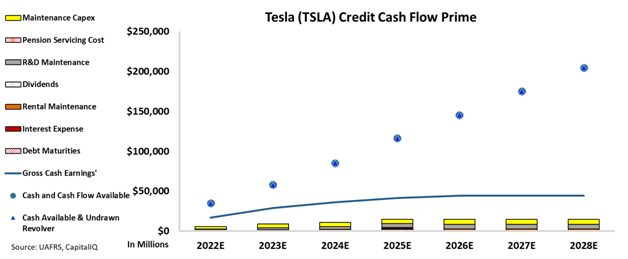

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (CCFP) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As evidenced by the following chart, Tesla has a much safer credit profile than the credit agencies have been suggesting. Its cash flows are perfectly sufficient to cover its obligations, let alone its building cash base.

The CCFP clearly shows that Tesla’s cash flow covers all the operating and financial obligations for the next five years and there is no real risk of default.

As a result, the company gets a sterling IG1 rating from Valens.

Looking at the whole picture, we can see at a glance the EV titan has a rock-solid balance sheet.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Tesla Tearsheet

As the Uniform Accounting tearsheet for Tesla, Inc. (TSLA:USA) highlights, the Uniform P/E trades at 58.0x, which is above the global corporate average of 19.7x, but below its historical P/E of 91.4x.

High P/Es require high EPS growth to sustain them. In the case of Tesla, the company has recently shown a 1,421% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Tesla’s Wall Street analyst-driven forecast is for a 111% and 37% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify TSLA’s $720 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 48% annually over the next three years. What Wall Street analysts expect for TSLA’s earnings growth is above what the current stock market valuation requires in 2022 but below in 2023.

Furthermore, the company’s earning power in 2021 is 3x the long-run corporate average. Also, cash flows and cash on hand are 4x its total obligations—including debt maturities and capex maintenance. Moreover, the company has an intrinsic credit risk that is 20bps above the risk-free rate.

Overall, this signals a low credit and dividend risk.

Lastly, TSLA’s Uniform earnings growth is well above its peer averages, and the company is also trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Tesla, Inc. (TSLA) credit outlook is the same type of analysis that powers our macro research detailed in the FA Alpha Pulse.