The pandemic has been a game-changer for a lot of industries.

Without a doubt, healthcare has been one of them. Both the companies focusing on research and the ones providing healthcare services have seen big changes in how they operate.

A lot of recognized increasing demand for services and enjoyed high profitability during the pandemic.

However, this high demand meant healthcare providers need more capacity. Combined with the aging population and retiring nurses, it quickly turned into a lack of workforce.

Now, it is clear that the U.S. needs more nurses.

The shortages are having a significant financial impact on hospitals. According to Fitch Ratings, operating margins at nonprofit hospitals shrank by five to seven percent.

Companies and the government are aware of this. Legislators on both state and federal levels are turning their attention to this issue.

The federal government already launched a $1.8 billion program to create 1,000 new residency slots at hospitals in under-served communities. The Biden administration allotted an additional $103 million from the American Rescue plan to improve retention for healthcare workers.

There is an effort for bipartisan legislation, aiming to train and attract more healthcare workers, particularly in rural areas.

Additionally, easing visa requirements for nurses is among the discussed topics.

While all this seems like an extra hassle for healthcare companies, there is one group of companies smiling—the staffing companies, particularly the ones working with hospitals.

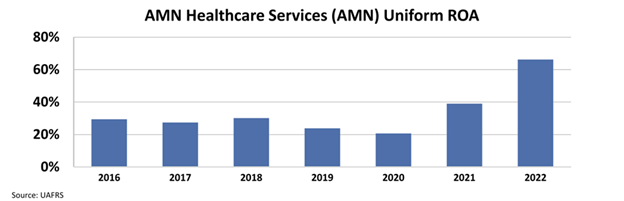

AMN Healthcare Services (AMN) is one of them. It provides healthcare workforce solutions and staffing services to hospitals and healthcare facilities in the U.S.

Just doing its core operations, it has seen immense demand for its services after the pandemic and enjoyed very high profitability.

Its return on assets (“ROA”) jumped from 21% in 2020 to 66% in 2022.

However, this does not lead us to an investment thesis. While the past two years has proved very profitable for the company, it doesn’t necessarily show that the name is an investment opportunity.

We need to understand what the market thinks about this name, so we can see if there is any mispricing.

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At $88 per share, the market expects AMN’s profitability to revert back to pre-pandemic levels.

Considering all that is going on in the healthcare staffing space, these expectations seem overly pessimistic.

Hospitals and healthcare facilities will have to work with staffing companies to cover the lack of nurses and AMN is in a strong position to benefit from this.

The story seems under the radar of the market for now, resulting in a possible upside opportunity.

SUMMARY and AMN Healthcare Services Tearsheet

As the Uniform Accounting tearsheet for AMN Healthcare Services (AMN:USA) highlights, the Uniform P/E trades at 12.5x, which is below the corporate average of 18.4x but around its historical P/E of 13.1x.

Low P/Es require low EPS growth to sustain them. In the case of AMN Healthcare, the company has recently shown a 65% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AMN Healthcare’s Wall Street analyst-driven forecast is a 26% EPS shrinkage in 2023 and a 2% EPS growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AMN Healthcare’s $86 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 16% annually over the next three years. What Wall Street analysts expect for AMN Healthcare’s earnings growth is below what the current stock market valuation in 2023 but above its requirement in 2024.

Furthermore, the company’s earning power is 11x its long-run corporate average. Moreover, cash flows and cash on hand are 4x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 290bps above the risk-free rate.

All in all, this signals average credit risk.

Lastly, AMN Healthcare’s Uniform earnings growth is in line with its peer averages and average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.