While startups are volatile, growth stocks, on the other hand, generate steadier profits and can focus more on business expansion. These companies generate enough cash to fuel growth, exceeding costs and rewarding investors. In today’s FA Alpha Daily, we’ll look at Uber from a “growth lens”, as it is way past its startup days.

FA Alpha Daily:

Friday Portfolio Analysis

Powered by Valens Research

Only 40% of startups can become profitable.

These profits are a byproduct of these companies’ ability to prove their products and services in the marketplace. Once the business model is accepted by the market, external funding may not be necessary as cash flows can provide the money for reinvestment.

This implies that ROA levels will gradually increase to a peak given that the business is no longer starting at subdued levels.

At the same time, while still robust, asset growth levels will tend to lower as the asset base begins to stabilize compared to when the company was still establishing its products.

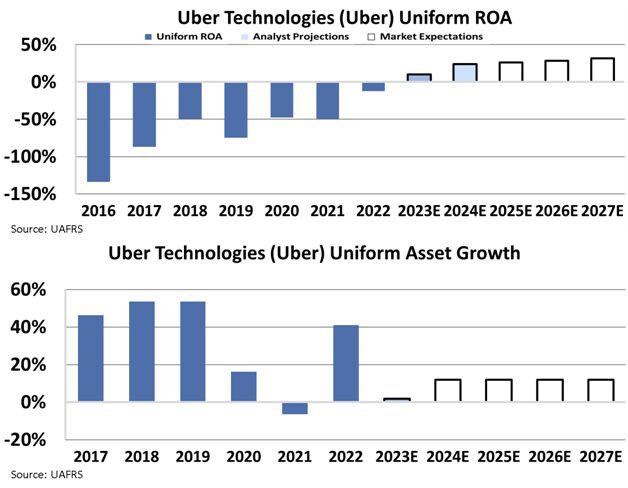

The negative to positive inflection is typically an indication that a business is entering this new stage, and this is exactly what we saw with Uber.

Despite an active user base of about $130 million, this ride-hailing giant didn’t yield a positive operating profit until Q2 of this year, after 14 years in business.

As the year comes to an end, analysts expect Uber to be around 10% ROA levels, with the market expectations of a sizable increase to about 31% in 2027.

Long story short, the market understands that Uber is beyond its startup days.

Take a look.

Uber’s new reputation as a money maker infers a few things.

Firstly, Uber’s asset growth will likely not be as robust and fluctuate as it was over the last 6 years. Moving forward, we expect growth to flatline around 12%.

In other words, the business will continue to grow but we aren’t expecting immense change and innovation like its earlier stages.

Secondly, such optimistic market expectations could limit the upside from a theoretical standpoint.

However, our research indicates the market may undermine the potential of growth companies like Uber.

Using the same 3,000-company universe we discussed last week, we mapped out the difference in the market’s expectations to the actual 5-year change in profitability.

Overall, it appeared that the market expected growth companies’ profitability to fade out more than they actually did. On average, the actual ROA change was 1.1% higher than market expectations.

This means that if a company is in its growth stage there is a good chance that these companies may outperform expectations.

As such, if investors can identify companies whose likelihood of fading is less than what is being priced in, they should be rewarded by a revaluation.

It’s too early to say the determine the future of Uber’s profitability, though this principle applies to this case. There are other components to consider when investing, but on a broader view, there is potential for Uber’s growth stage to exceed the fading that the market factors in.

That being said, this will not hold in all cases, but the trend is there. Investing in this manner would require an investor to identify a company that has a reason to beat the “fade.”

This is the second part of a five-part series on the business life cycle, and the next article will detail what happens when a company is done growing and begins to “mature.”

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This portfolio analysis highlights the same insights we share with our FA Alpha Members. To find out more, visit our website.