Even as the S&P 500 struggles with tariffs, inflation, and weak confidence, Palantir’s stock has soared. Its business is booming, but the market’s sky-high expectations leave no room for error. In today’s FA Alpha Daily, we dive into why Palantir’s stellar performance wasn’t enough—and what its valuation says about future risks.

FA Alpha Daily

Powered by Valens Research

Since the start of the year, the S&P 500 has struggled under a cloud of uncertainty.

Early gains faded as fresh rounds of tariffs on key trading partners drove costs higher and rattled corporate supply chains.

Investors worried that higher import prices would squeeze margins and that retaliatory measures abroad could slow global growth.

At the same time, inflation has held above the Fed’s 2% target, keeping interest rates elevated and putting pressure on valuations across the board.

Business and consumer confidence dipped, and the index sits roughly 5% below its January level.

Despite everything going on with the economy, Palantir (PLTR) managed to stand out.

Its stock has climbed about 45% year-to-date, even after a pullback following its latest earnings report.

Palantir’s latest quarter delivered everything the market wanted to hear. Revenue grew by nearly 40% year-over-year, margins expanded and the company lifted its full-year guidance.

On the surface, that should have sent the stock higher. Instead, shares slid more than 10% after the report.

That reaction speaks to just how high expectations have climbed and how little room there is for any slip, even when the underlying business is firing on all cylinders.

Palantir’s platform is winning new customers and convincing existing ones to spend more. In Q1, total revenue hit $880 million, led by a 71% jump in U.S. commercial sales and a 45% gain in government contracts.

Commercial users alone are now running at a $1 billion annual pace in the U.S., evidence that companies outside of defense and intelligence are finding real value in Palantir’s data tools.

That’s what drove management to nudge full-year revenue guidance up to roughly $3.9 billion, a 36% increase over last year.

As-reported profitability is improving alongside growth. Adjusted gross margins remain in the low-80s, while free cash flow margins topped 40% for the quarter.

Palantir isn’t just piling on low-margin clients; it’s selling software that sticks. And with operating leverage kicking in, every additional dollar of revenue now contributes more to the bottom line.

Taken together, those numbers would be satisfying for most software companies. They certainly met and beat the street’s projections.

What rattled investors was the valuation.

At current prices, Palantir trades at more than 440x forward Uniform P/E, an extraordinary premium even in today’s AI market.

For context, peers like Microsoft (MSFT) and Salesforce (CRM) trade around 25x Uniform earnings.

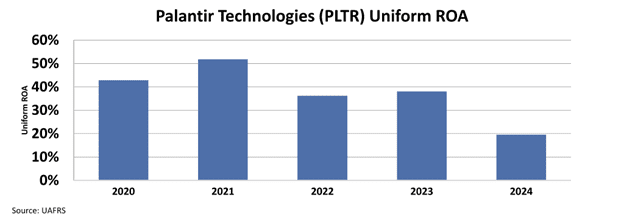

Palantir’s Uniform return on assets ”ROA” was around 20% in 2024, not that impressive for a fast-growing software business and hardly supports such a steep multiple.

The market clearly believes nothing short of perfection will justify that price.

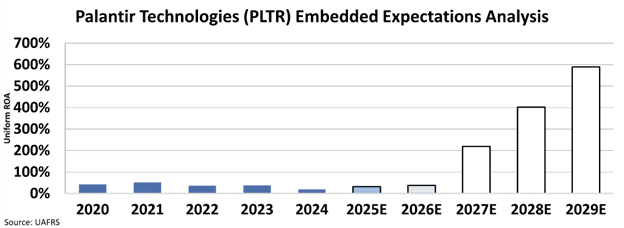

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s Uniform ROA to skyrocket to around 590% from 20% last year.

When a company already priced for perfection delivers excellent execution, there’s nowhere for the stock to go but down unless it exceeds the already lofty bar.

And while Palantir’s long-term story remains compelling, with continued adoption of its AI-driven Foundry and AIP platforms and potential to expand into new industries, short-term swings are likely to be sharp.

Any hint of slower-than-expected customer wins or softer spending could trigger more selling.

Investors should be careful when investing in a company that is already priced for perfection.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.