Trucking occupies a big portion of tonnage across all modes of freight transportation, representing roughly 73%. And in 2024, trucks hauled approximately 11.2 billion tons of freight.

The logistics industry enjoyed a strong 2020. Shifting consumer habits away from services to physical products due to COVID restrictions, as well as larger supply chain fragilities drove up freight demand and trucking rates.

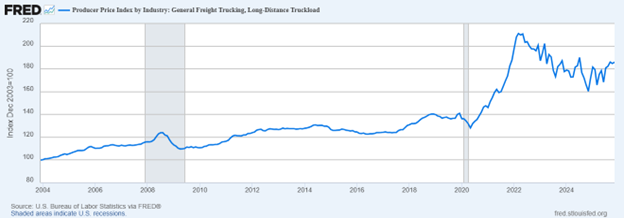

The Producer Price Index for long-distance freight trucking reflects this dynamic. Shortly after the onset of the pandemic, the index rose from 128 to 211 by early 2022, an all-time high.

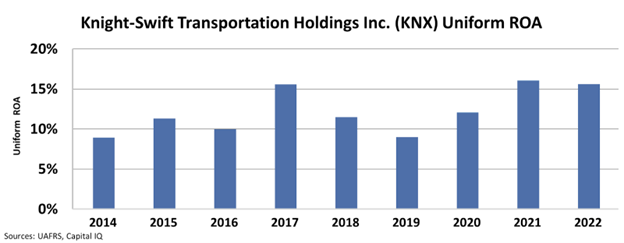

This was a historically strong cycle for the logistics industry, and trucking leader Knight-Swift (KNX) reaped the benefits. The company’s Uniform return on assets (“ROA”) rose to a record 16% in 2021, which it sustained in 2022.

However this cycle quickly turned for the worse for Knight-Swift and the rest of the logistics industry.

Due to the trucking industry’s pricing power over manufacturers and sustained demand for logistic services during the pandemic, the trucking industry saw an influx of companies and drivers eager to meet this demand.

At the end of 2019 there were around 4.5 million drivers with commercial drivers licenses in the United States. By the end of 2022 this figure rose to 5.4 million drivers.

As new drivers took to the roads the logistics industry soon found itself oversupplied.

The Producer Price Index for long-distance freight trucking is down from its 211 heights in 2022 to 186 today.

The declining power of freighters over manufacturers caused an exodus of tens of thousands of trucking companies and hundreds of thousands of drivers. Still, there are around 300,000 more commercial drivers today than before the pandemic.

Knight-Swift has survived the cycle downturn, however returns have fallen to historic lows over the past two years.

After generating an average ROA of 13% between 2015 and 2022, returns cratered to just 4% in 2024.

And recent earnings suggest the company is struggling to replicate its previous success in the current market.

During its earnings call for the fourth quarter of 2025, the company reported a loss of $6.8 million in contrast to a profit of $69 million in the prior year. Meanwhile, revenue dipped to $1.86 billion, narrowly missing analyst estimates of $1.89 billion.

The company’s truckload segment—its largest business unit—saw its revenue decline 2.4% year-over-year. Knight-Swift’s CEO, Adam Miller, said that the company’s truckload unit experienced lower demand in the quarter partly due to seasonal project activities not lasting longer compared to previous years.

Knight-Swift’s shares fell by nearly 5% following its earnings call. The company expects that conditions for the first quarter of 2026 will remain stable.

Knight-Swift still has a ways to go before delivering returns that match its historical performance. Until rates improve and the wider logistics industry shows lasting recovery, companies like Knight-Swift would be best to avoid for investors.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.