The U.S. is in the middle of an infrastructure investment boom driven by the AI revolution, grid modernization, and government-backed initiatives.

The bipartisan 2021 Infrastructure Investment and Jobs Act has so far, awarded $570 billion has already been awarded to various infrastructure projects. The bill’s purpose is to infuse capital into various roads, bridges, power infrastructure, public transportation, and other related projects.

Meanwhile, Big Tech is expected to spend over $700 billion on data centers in 2026. Since the latter requires gargantuan amounts of energy, efforts are underway to modernize America’s aging power grid—an undertaking that’s estimated to require over $1 trillion in funding.

In addition to grid modernization efforts, alternative energy sources such as solar and wind continue to see interest and investment despite regulatory headwinds. In 2025, wind accounted for 10% of newly added energy sources.

Companies with exposure to these infrastructure-related tailwinds are positioned to benefit. And among them is Arcosa (ACA).

Arcosa is a company that caters to the construction and engineered structure markets.

At present, the company operates two major business segments: Construction Products and Engineered Structures.

The Construction Products segment operates businesses involved in natural and recycled aggregates which includes sand, gravel, and limestone mines operations, concrete recycling and other construction materials, and stabilized sand.

Arcosa’s aggregates business operates across multiple states including Arizona, Texas, Louisiana, Mississippi, Pennsylvania, New Jersey, and Kentucky.

The Construction Products segment also processes and distributes lightweight aggregates, plaster products, gypsum, and other downstream food and building materials. Lastly, this segment specializes in producing and distributing steel and aluminum trench shoring and shielding equipment.

On the other hand, the Engineered Structures segment services a wide array of end markets including electricity transmission and distribution, lighting, wind power, traffic structures, and wireless communications.

Arcosa has shed some parts of its businesses in recent years. It sold its storage tank and steel businesses in 2022 and 2024, respectively. And recently, it sold its barge business earlier this year.

These strategic moves have enabled the company to focus on its construction and engineered structure businesses.

Construction Products generated 62% of the company’s revenue in 2025, with Engineered Structures generating the rest.

Aside from shedding businesses, the company has turned to acquisitions to boost its portfolio. In 2024, it acquired Stavola, a construction materials firm.

Through these strategic moves over the years, Arcosa has transformed itself into an infrastructure-focused powerhouse that is favorably positioned as a “picks and shovels” play on U.S. infrastructure and grid modernization.

And since aggregates are expensive to move across different locations, the company also enjoys pricing power in the areas where its business operates.

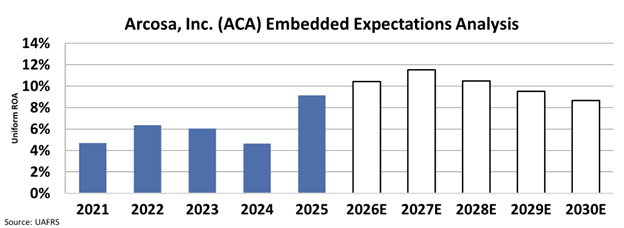

Despite this, investors are underestimating Arcosa’s overall business and transformation in recent years. We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Investors expect the company to generate a Uniform return on assets (“ROA”) 10% by 2030, just slightly higher than the 9% Uniform ROA the company delivered in 2025.

This valuation suggests that investors are underestimating the impact of Arcosa’s transformation.

Given the company’s exposure to the tailwinds brought by America’s reindustrialization and grid modernization, it should be positioned to grow its returns further, enabling it to meet or even exceed market expectations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.