Many praise investors who take risky bets and win big, but Warren Buffett is known for doing the opposite. Today’s FA Alpha Daily will reveal what opportunities Warren Buffett spotted through Berkshire Hathaway’s (BRK.A) three massive investments after years of not making any big moves.

FA Alpha Daily:

Thursday Uniform accounting analysis

Powered by Valens Research

The media, and society by extension, often laud those that take risky bets and win big.

In the finance industry, there is an investor that has made his name as one of the greatest to ever do it by doing the exact opposite.

Warren Buffett, or the “Oracle of Omaha” as he is fondly called for what seems to be an uncanny vision into future winners, is a notoriously judicious capital allocator.

While many professional investors are constantly chasing their next Moby Dick, or “whale” of an investment, Buffett takes the approach of saying no to almost every idea that crosses his desk.

Just as the analysts that pour incessant hours into preparing these ideas may feel, this cautiousness can be frustrating at times for him.

In his most recent annual Berkshire Hathaway (BRK.A), Buffett wrote that through 2021, there was “little that excites us”, in reference to his longtime business partner Charlie Munger.

It’s precisely his willingness to step back and say “no” when he doesn’t find anything interesting that makes his moves that much more meaningful.

After an extended period of stepping back from making any large moves, it seems he is finally ready to change his tune.

With interest rates rising and the markets experiencing elevated volatility from Russia’s invasion of Ukraine, Berkshire is finally making moves.

Buffett recently announced Berkshire Hathaway was buying the reinsurer Alleghany for $11.6 billion, marking the company’s biggest acquisition in years.

However, he didn’t stop there, as soon after, he added a large slug of equity in Occidental Petroleum (OXY).

And just yesterday, he announced a $4.2 billion stake in HP Inc. (HPQ), representing an 11% stake in the company.

Three investments of this size don’t happen every day at Berkshire, so it’s a critical sign that Buffett is finally seeing an oversold market with some interesting opportunities.

As such, it’s time we use Uniform Accounting to review Berkshire’s top holdings to see what the Oracle likes these days.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It is no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in reality robustly profitable and which may not be as strong of an investment.

Just as one would expect from someone who is called an Oracle, Warren Buffet’s portfolio is much stronger than the as-reported metrics dictate.

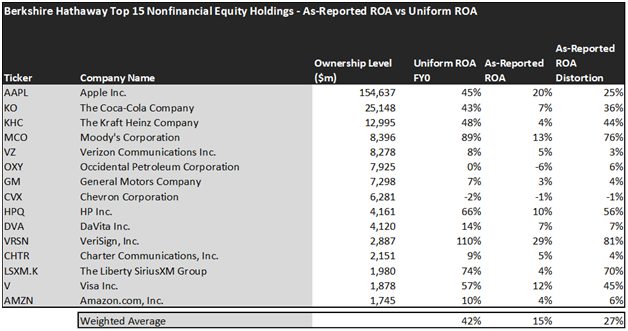

The average as-reported ROA among Berkshire’s top 15 names is a solid, albeit slightly unimpressive 15%. In reality, though, these companies are massively profitable on average, with a 42% Uniform ROA across the top 15.

The Coca-Cola Company (KO), his longest-held investment, for example, doesn’t return a below average 7%. Rather, as a company with a strong portfolio of products, it has a 43% Uniform ROA.

Some of Berkshire Hathaway’s other investments are also much stronger than they appear. For example, Moody’s Corporation (MCO) does not have 13% returns. It returns 89% because its assets are much more efficient than as-reported metrics suggest.

However, it isn’t just his old investments that sparkle when examined. The Liberty SiriusXM Group (LSXM.K) doesn’t have returns below cost of capital returns of 4%. Rather, it has dramatically stronger returns of 74%.

Largely, once we account for Uniform Accounting adjustments, we can see that many of these companies are strong stocks that have unfairly been beaten down by the market.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

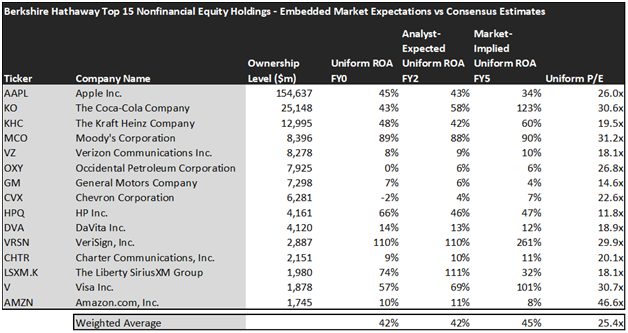

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The Uniform ROA FY0 represents the company’s current return on assets, which is a crucial benchmark for contextualizing expectations.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here is 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, average Uniform P/E across the investing universe is roughly 24x.

Embedded Expectations Analysis of Berkshire Hathaway paints a clear picture of the fund. The stocks it tracks are companies with strong fundamentals and robust cash flows that typically allow for high dividend payments.

Analyst expectations are pricing these companies to keep their economic profitability at 42%. Meanwhile, the market have them rising slightly to 45%.

While the portfolio as a whole appears to be accurately priced, there are still some significant distortions that could lead to massive upside or disappointment.

Some companies like Occidental Petroleum Corporations (OXY) and Verizon Communications (VZ), are very accurately stated with both analysts and markets agreeing on their Uniform ROAs.

However, the story changes once we dig into some of their other holdings.

Although The Coca-Cola company has served him very well for years, the market appears to think that it is in a stronger position with expectations of 123% versus analyst expectations of some growth to 58%.

A company like The Liberty SiriusXM Group (LSXM.K) might come in to save the day again this time though. With the market expecting returns to crash to 32%, analyst expectations of a 111% Uniform ROA provides the opportunity for a strong upside.

This just goes to show the importance of valuation in the investing process. Finding a company with strong fundamentals is only half of the process. The other, just as important part, is understanding just how much more upside the company has left in them.

To see a list of companies that have great performance and future upside also at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of the largest holding in AAPL.

SUMMARY and Apple Inc. Tearsheet

As Berkshire Hathaway’s largest individual stock holdings, we’re highlighting Apple Inc.’s (AAPL:USA) tearsheet today.

As the Uniform Accounting tearsheet for Apple Inc. highlights, its Uniform P/E trades at 26.0x, which is above the global corporate average of 24.0x and its historical average of 20.4x.

High P/Es require high EPS growth to sustain them. In the case of Apple, the company has recently shown a Uniform EPS growth of 72%.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Apple’s Wall Street analyst-driven forecast is for EPS to grow by 7% and 3% in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Apple’s $175 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 8% annually over the next three years. What Wall Street analysts expect for Apple’s earnings growth is below what the current stock market valuation requires through 2023.

Meanwhile, the company’s earning power is 7x the long-run corporate averages. Also, cash flows and cash on hand are 3x total obligations—including debt maturities and capex maintenance. Moreover, intrinsic credit risk is 20 bps. Together, these signal low dividend and credit risks.

Lastly, Apple’s Uniform earnings growth is below its peer averages, but is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This portfolio analysis highlights the same insights we use to power our FA Alpha product. To find out more visit our website.