Fair Isaac Corporation (FICO), the company behind the FICO score, recently sent shockwaves throughout the $13 trillion mortgage market when it unveiled a new licensing plan that effectively lets mortgage lenders acquire credit scores more easily, bypassing credit bureaus entirely.

Prior to this announcement, mortgage credit specialists, known as tri-merge resellers, had to buy FICO scores from Experian (LSE:EXPN), TransUnion (TRU), and Equifax (EFX)—the three largest credit bureaus—to supply lenders with a FICO score.

The move won’t deem the credit bureaus irrelevant, since lenders still need these firms for credit reports and their vast pool of consumer data.

But it will make the process of acquiring credit scores more efficient, and cheaper for lenders. Under the new program customers can purchase scores for the same rate it charges credit bureaus, plus an additional fee when a loan closes.

This saves lenders from the high mark ups passed on by the large bureaus.

Even though this new program is limited to mortgages, analysts speculate the model could extend to other borrowing segments if successful.

FICO’s shares are up 21% since announcing the new licensing model. Meanwhile, shares of Experian, TransUnion, and Equifax are down 5%, 10%, and 7%, respectively.

FICO’s new model has the potential to transform how investors look at the credit-score market, as some analysts predict it could erase 10% to 15% from the big bureaus’ earnings.

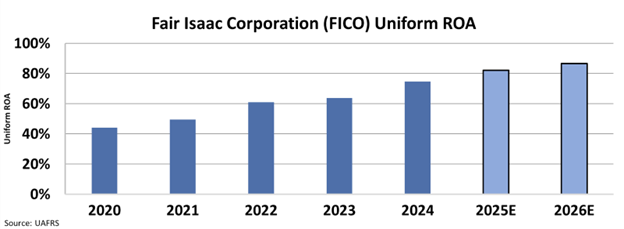

Conversely, this could give FICO another boost following years of accelerating returns. Since 2020, the company’s ROA has risen from 44% to 75%, and Wall Street analysts believe its returns could reach 87% by 2026.

By offering its credit scores directly to lenders, FICO has cut out the middleman and opened the doors for a significant uptick in volume, which should translate into higher returns for the company.

Conversely, the big credit bureaus are under unexpected pressure now. It remains to be seen what the total impact of FICO’s move will be, however it does pose a cautionary lesson for investors.

No matter how deeply entrenched big players are in their respective industries, companies are rarely immune to disruption.

It is imperative for any investor to identify the risks within a business, and understand the potential windfalls before making any investment decision.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.