Yesterday, we talked about IT consultant Garner (IT) and explained how its second quarter earnings call led to its stock price to decline more than 25%.

Even though it achieved positive results in its most recent quarter, its stock went spiraling down after management lowered its full-year revenue guidance to $6.45 billion, below consensus estimates which were closer to $6.54 billion.

This guidance change altered how the market thinks about the IT consultant, leading to its subsequent sell off.

Earnings calls can lead to vast stock movements as these quarterly meetings are some of the only times company leadership can communicate with shareholders over the course of the year.

If anything discussed in these calls fail to meet or exceed expectations, the market can adversely react, leading to the decline experienced by Gartner.

While the IT consultant suffered as a result of lowered guidance, sometimes stocks fall short even in the face of seemingly positive earnings calls. AI-lending platform Upstart’s (UPST), strong quarterly results weren’t enough to satisfy investors, and they punished the company for failing to meet their lofty expectations.

Upstart is a lending platform that leverages AI- and machine learning-powered models to assess a borrower’s credit status.

Instead of relying on FICO scores and other traditional indicators, the platform evaluates borrowers based on unconventional factors such as educational attainment, job history, and income.

Its models are trained on millions of monthly repayment events to identify and predict if borrowers have the means and discipline to repay loans and how likely they are to default.

The company, through its AI-powered platform, works with banks and credit unions to assess borrower creditworthiness and improve credit access while minimizing the risk and costs of lending for its partners.

On August 5th, Upstart announced its much-awaited second quarter 2025 results.

The company generated $257 million in revenue, achieving a 102% YoY growth, beating expectations by nearly 14%. Furthermore, management raised revenue guidance 4.5% for 2025.

Moreover, loan originations more than doubled, rising from $1.1 billion to $2.8 billion during the second quarter of 2025. Loan conversion rates are up by nearly 24% as well.

All in all, these numbers indicate Upstart has been executing its strategy and effectively grown its business.

Despite this, the company’s stock price declined.

Since earnings were released on Tuesday, the company’s stock price dropped by more than 15%, a surprising response from a market that’s just seen strong results.

However, this reaction becomes clearer to understand when we consider investors’ bullish projections for this business.

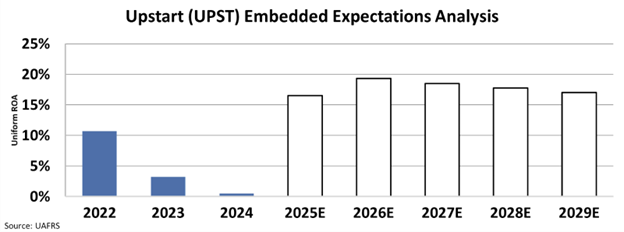

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

In the chart above, the white bars represent the market’s expectations for the company.

At the current stock price, the market expects Upstart’s Uniform return on assets (“ROA”) to rise from just 0.5% in 2024 to 17% by 2029.

These ROA expectations are high considering the company has failed to achieve similar levels in recent years.

Upstart would need to improve upon its recent momentum for upcoming quarters to satisfy these sky-high expectations. And since its business is dependent on lenders and borrowers, its performance is susceptible to economic headwinds that can impact borrowing.

Another factor to consider is that the loans held by the company rose 24% over the past year, from $821 million in the second quarter of 2024 to over $1 billion in the second quarter of 2025.

These loans present additional risk for the business as its loans, which it uses for R&D purposes to train its model, could significantly disrupt the business in the event of a greater-than-expected number of defaults.

Upstart may have had a good quarter on the surface, but when market expectations are taken into consideration, this business still has a lot to achieve.

As long as the market continues to expect transformative results from this company, upside may be difficult to come by for investors.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.