Back in February 2021, we were still in the depths of the pandemic lockdowns. Hotels sat empty, and flights were running with only a few seats filled. Thanks to government-enforced lockdowns, events like concerts and comedy shows were almost nonexistent.

For the ticket vendor and venue manager Live Nation Entertainment, revenue was slashed thanks to government mandates. For a company selling live events, every lost dollar was ‘permanent.’ It was impossible for Live Nation to be making up the lost revenue from every month the lockdown went on.

When the pandemic was at its height, Moody’s gave the company a B2 rating, indicating a high chance of default.

However, the company was able to sustain its operations and payroll thanks to its smart balance sheet management. We highlighted back in February that the company was in a strong position to weather the downturn thanks to its debt load not coming due until 2023 and beyond.

Now, more than a year later, Moody’s still gives Live Nation a B2 rating, which corresponds to a default rate of over 25%. Not only was this rating out of touch during the pandemic, while the company smartly managed its debt load, but it is even more far fetched today.

As concerts have come back in force and pent-up demand is being released across the country, Live Nation has used its strong cash flows to refinance its debt out even further into the future while drawing down its interest expense.

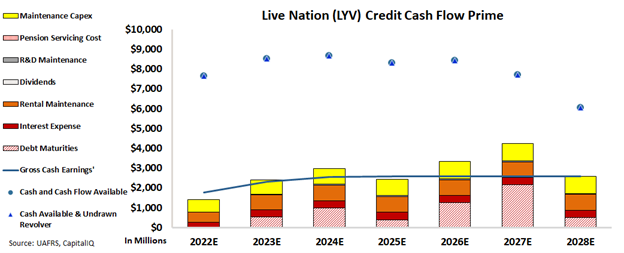

We can see exactly how safe the name is by examining it through the Credit Cash Flow Prime perspective.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The B2 rating suggests a high risk of default, but the CCFP shows that Live Nation’s cash on hand is more than enough to cover all of its obligations over the next seven years.

Considering how Live Nation has been continuing to improve its credit picture over time, it’s ludicrous that the ratings agencies like Moody’s are still this far behind the picture.

That is why it deserves to be a crossover XO- rating, which corresponds to a default risk of around 10%.

Rating agencies seem to miss the potential of successful companies again, by rating Live Nation much riskier than the company actually is.

On the other hand, Valens Credit Rating reflects the full story of the company with much less risk than what the rating agencies suggest.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Live Nation Entertainment Tearsheet

As the Uniform Accounting tearsheet for Live Nation Entertainment, Inc. (LYV:USA) highlights, the Uniform P/E trades at 27.5x, which is above the global corporate average of 18.4x and its historical P/E of -41.0x.

High P/Es require high EPS growth to sustain them. In the case of Live Nation, the company has recently shown a 70% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Live Nation’s Wall Street analyst-driven forecast is for a 234% EPS shrinkage in 2022 and a 13% EPS growth in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Live Nation’s $69 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2021 is below the long-run corporate average. Yet, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. However, the company has an intrinsic credit risk that is 160bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, Live Nation’s Uniform earnings growth is well below its peer averages, but the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Live Nation Entertainment, Inc. (LYV) credit outlook is the same type of analysis that powers our macro research detailed in the member-exclusive FA Alpha Pulse.