Coal is a hated business by credit and equity investors alike, as future expectations are for the industry to continue to be phased out for cleaner energy and green energy solutions.

However, contrary to what credit rating agencies may believe, that doesn’t mean that these coal companies are going under tomorrow especially with the recent spike in coal prices.

Furthermore, few coal companies that are still operating today are under the delusion that their businesses will last forever. This is why most of them are doing smart things with their money such as investing in alternative energy when they make surplus returns. That’s exactly what Arch Resources is doing.

The credit rating agencies are blind to the good years Arch Resources still has ahead, along with its alternative investment. S&P has given the company a B- credit, firmly placing the company in high-yield status. This means the company should have less more than a 10% chance of default over the next ten years.

However, we don’t see things the same way here at Valens.

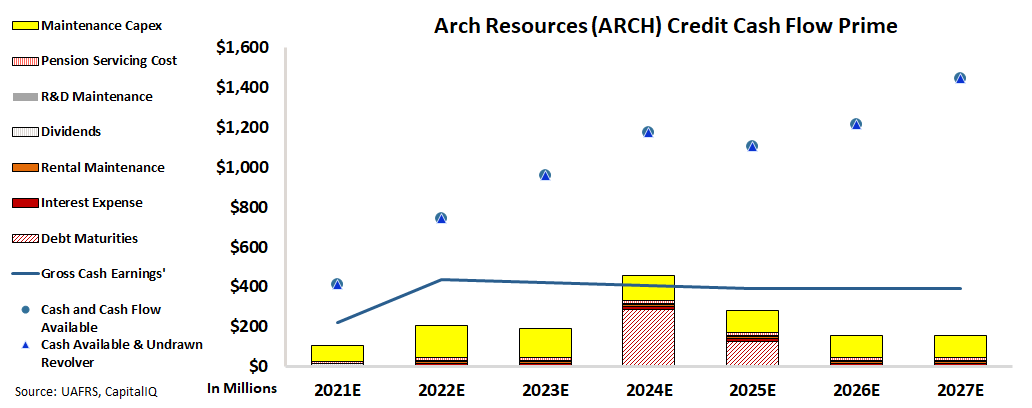

Using our Credit Cash Flow Prime (“CCFP”) framework, we can get to the heart of Arch Resources’ true fundamental credit risk.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As you can see, Arch Resources is able to cover all of its operating obligations with its cash flows alone for the next seven years. Furthermore, it is building a sizable amount of cash on its balance sheet, which means it should have no issue whatsoever with paying off its debt obligations in 2024 and 2025 with excess funds on its balance sheet.

Not only is Arch Resources not anywhere close to financial troubles, but it also has plenty of capital to invest away from coal and become an energy company of the future in the next decade.

S&P’s B- high-yield rating for Arch Resources does not reflect reality. Instead, it highlights Wall Street’s blindness to true credit risk.

That’s why we rate the company as having a much lower risk with an investment-grade rating of IG3, which corresponds to a default rate of less than 2%.

Using Uniform Accounting, we can see through the distortions of as-reported numbers to get to the true fundamental credit picture for companies in transition such as Arch Resources.

To see Credit Cash Flow Prime ratings for thousands of other companies we cover, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Arch Resources, Inc. Tearsheet

As the Uniform Accounting tearsheet for Arch Resources, Inc (ARCH:USA) highlights, the Uniform P/E trades at 3.2x, which is below the global corporate average of 24.0x, but around its historical P/E of 2.2x.

Low P/Es require low EPS growth to sustain them. In the case of Arch Resources, the company has recently shown a 198% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Arch Resources’ Wall Street analyst-driven forecast is a 307% EPS decline in 2021 and 100% growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Arch Resources’ $87 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power is below the long-run corporate average. Moreover, cash flows and cash on hand are more than 5x its total obligations—including debt maturities and capex maintenance. All in all, this signals an average credit and dividend risk.

Lastly, Arch Resources’ Uniform earnings growth is below peer averages, and the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Arch Resources, Inc credit outlook is the same type of analysis that powers our macro research detailed in the FA Alpha Pulse.