LGI Homes, Inc. (LGIH) became fully valued after its rapid stock appreciation as a result of the rising house demand and firm expansion, yet credit markets seemed to have missed the picture. Today’s FA Alpha Daily will examine LGI Homes’ credit risk with the Credit Cash Flow Prime.

FA Alpha Daily:

Wednesday Credit

Powered by Valens Research

One of our favorite stock picks through the middle of 2021 was LGI Homes (LGIH).

It experienced rapid stock appreciation as the booming demand for homes combined with its company-specific growth tailwinds of management grew the business into new, higher-demand regions.

We stopped recommending the company because the stock became fully valued, as the market realized just how great of a company it was.

As the saying goes though, all good things come to an end.

Or so we thought.

Apparently, the credit ratings agencies have completely missed LGI Homes’ huge run of cash flows and growth throughout the housing boom of 2020 and beyond.

With a high yield (BB-) rating and a 10% risk of default, credit markets continue to think LGI Homes is as safe as a shack in a tornado.

Instead, the company’s impressive cash scale and cash flow generation, alongside continued booming macroeconomic tailwinds, say it’s more like a tornado shelter.

For these reasons, LGI Homes’ Credit Cash Flow Prime (CCFP) is way healthier than the market is thinking.

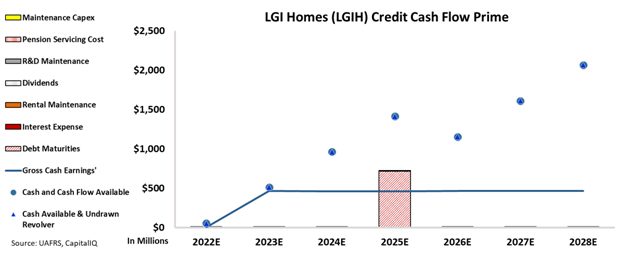

We can figure out if there is a real risk for this high-potential company by leveraging the CCFP to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Its BB- rating suggests a high risk of default, but the CCFP shows that LGI’s cash flows cover all of its miniscule operating obligations until 2026, when its large cash reserve will handily cover its 2025 debt.

That’s why the Valens Credit Rating for the name is a much stronger IG4.

Even though all operating obligations are covered by cash flows, ratings agencies continue to discredit them because of their massive debt headwall in 2025.

On the contrary, Valens Credit Rating represents the full story of the company. LGI Homes has a lot less risk attached to it than what the rating agencies suggest.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and LGI Homes, Inc. Tearsheet

As the Uniform Accounting tearsheet for LGI Homes, Inc. (LGIH:USA) highlights, the Uniform P/E trades at 7.2x, which is below the global corporate average of 24.0x, but around its historical P/E of 8.0x.

Low P/Es require low EPS growth to sustain them. That said, in the case of LGIH, the company has recently shown a 36% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, LGIH’s Wall Street analyst-driven forecast is for a 6% EPS shrinkage in 2022 and a growth of 6% in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify LGIH’s $98 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to decline by 16% over the next three years. What Wall Street analysts expect for LGIH’s earnings growth is below what the current stock market valuation requires in 2022 and 2023.

Furthermore, the company’s earning power in 2021 is 3x the long-run corporate average. Moreover, cash flows and cash on hand are more than 3x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low dividend risk.

Lastly, LGIH’s Uniform earnings growth is well below its peer averages, but the company is trading around its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of LGI Homes, Inc. (LGIH) credit outlook is the same type of analysis that powers our macro research detailed in the FA Alpha Pulse.