One of the industries that was significantly affected by the pandemic was coal mining. Due to restrictions, lockdowns, and declining demand, profitability dipped in 2020.

In this environment, they had to support their operations by taking on debt, which is what Peabody Energy (BTU) did at the time.

Now that coal has become more important with the emergence of an energy crisis happening in Europe, Peabody is prepared to enjoy rising demand.

The company paid the majority of its obligations last year and is now well-positioned to take advantage of the current market conditions.

The rising demand and short-term profitability may be good news for the company but the sustainability of coal remains highly debatable.

However, it’s not what credit investors care about.

Investing in a company’s credit or equity may look alike for some people, but there are incremental differences between these two securities.

While equity investors focus on a company’s profitability or growth, credit investors care about the company’s ability to pay its debt.

What’s important for credit investors while thinking about Peabody Energy should be the amount of debt the company paid.

The company retired all of the $545 million of senior secured debt during the fourth quarter of last year and significantly reduced its total debt.

Due to the challenges in 2020, its total debt rose to around $1.6 billion, but the company showed great resilience in managing it and reduced it to around $360 million by the end of 2022.

However, it looks like rating agencies didn’t get the memo. Apparently, they failed to see the significant amount of debt repaid by the company and gave them a rating with an unbelievable chance of bankruptcy.

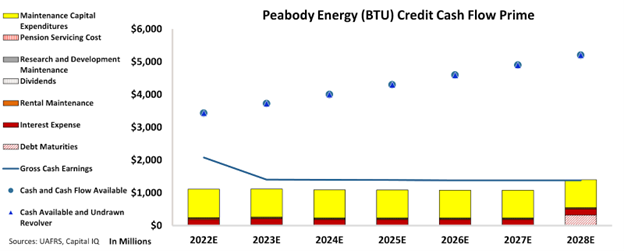

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Peabody Energy’s cash flows are much higher than its obligations going forward.

CCFP chart indicates that the company has very limited debt maturities and has a ton of cash to easily pay all of its obligations in the next few years.

In this case, it does not look like the company has a significant credit risk.

Yet, credit rating agencies like S&P think differently and rate the company “B” which implies around a 25% chance of default.

Our opinion does not align with the rating agencies and we understand Peabody’s efforts in debt repayments and its work towards a healthier balance sheet.

Hence, we think that even in the worst-case scenario, the company deserves a “XO” credit rating from Valens. This rating implies just around a 2% chance of default as opposed to 25% from rating agencies.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Peabody Energy (BTU:USA) Tearsheet

As the Uniform Accounting tearsheet for Peabody Energy (BTU:USA) highlights, the Uniform P/E trades at 8.0x, which is below the global corporate average of 18.4x but above its historical P/E of -1.9x.

Low P/Es require low EPS growth to sustain them. In the case of Peabody Energy, the company has recently shown a 40% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Peabody Energy’s Wall Street analyst-driven forecast is for a 228% and 68% EPS shrinkage in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Peabody Energy’s $26 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2021 was below the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 210bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, Peabody Energy’s Uniform earnings growth is below its peer averages and is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Peabody Energy (BTU) credit outlook is the same type of analysis that powers our macro research detailed in the member-exclusive FA Alpha Pulse.