Corporate actions such as spin-offs, re-organizations, and M&As are critical strategic maneuvers that can significantly impact a company’s profitability, growth, and efficiency. As these actions hold great importance for investors, comprehending a company’s prospects post-transaction can be a challenging task. Pediatrix Medical Group (MD) faced this challenge following its spin-off in 2020, with credit markets misconstruing the company’s credit risk. In today’s FA Alpha Daily, we will look at Pediatrix Medical Group (MD) by utilizing Uniform Accounting to evaluate the company’s actual profitability about its obligations and make an informed decision regarding the true risk of the business.

FA Alpha Daily:

Wednesday Credit

Powered by Valens Research

When a company conducts a spin-off on one part of its business, the aim is usually to increase profitability or efficiency.

This complicates things for investors since this action could significantly affect the company’s future for better or worse, and there are always risks involved in these major transactions.

That is why spin-offs and re-organizations can be noisy due to a misunderstanding from both equity and credit markets.

This is what exactly Pediatrix Medical Group (MD), a health care services company, has been experiencing in the last two years.

The company had two main businesses before the spin-off: pediatrics and radiology services.

In 2020, Pediatrix sold the radiology business for around $885 million to solely focus on its highly successful pediatrics and obstetrics businesses.

The company aimed to increase efficiency and focus with this transaction and also used the proceeds to reduce its debt burden.

After the transaction, the company also changed its name from Mednax to what it was initially founded as the Pediatrix Medical Group.

The changes in its name, executive team, and businesses made investors worried.

However, as opposed to what investors have been worried about, the company was able to mitigate the risks of the transaction and reached its goals towards a healthier balance sheet.

Yet, credit markets and rating agencies seem to still be misunderstanding the business as they give a very high credit rating for the company.

S&P thinks that Pediatrix can go to bankruptcy with a 10% chance, which is too much credit risk considered for the company.

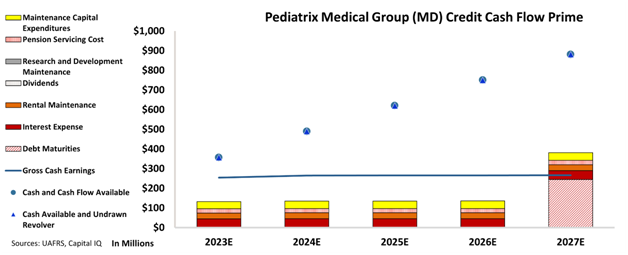

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart clearly shows that Pediatrix Medical Group’s cash flows are more than enough to cover its obligations going forward.

CCFP chart indicates that the company has a debt headwall in 2027 but there’s plenty of time to refinance that debt load.

Also, the company’s cash and cash flow available are much higher than its debt burden and other obligations.

Considering these factors, Pediatrix actually does not look like a company with a significant credit risk. Instead, the company is looking pretty safe in terms of credit risk.

That is why, as opposed to S&P’s incredibly high rating, we are giving an “IG3-” rating to the company, which implies around a 1% chance of default.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here o learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Pediatrix Medical Group (MD:USA) Tearsheet

As the Uniform Accounting tearsheet for Pediatrix Medical Group (MD:USA) highlights, the Uniform P/E trades at 18.3x, which is around the global corporate average of 18.4x but below its historical P/E of 19.4x.

Low P/Es require low EPS growth to sustain them. In the case of Pediatrix, the company has recently shown a 52% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Pediatrix’s Wall Street analyst-driven forecast is for a -31% and 12% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Pediatrix’s $14 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2022 was 5x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 470bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, Pediatrix’s Uniform earnings growth is below its peer averages and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Pediatrix Medical Group (MD)’s credit outlook is the same type of analysis that powers our macro research detailed in the member-exclusive FA Alpha Pulse.