The Trump administration is leaning into affordability ahead of the 2026 midterm elections.

President Donald Trump visited Michigan this month with a political goal that’s easy to understand.

He wants Republicans to keep control of Congress, and he wants voters focused on cost of living.

That’s why his team has been floating a series of populist ideas since the new year, including caps on credit card charges.

Trump’s visit is his third to a bellwether state since early December, and it comes as voter frustration builds. In a Detroit News survey cited in Bloomberg, nearly two-thirds of likely Michigan voters said household costs rose over the past year, with more than 80% pointing to groceries.

In that environment, credit cards are entering the political sphere. Trump pushed for all card issuers to implement a 10% interest rate cap, far below where the market sits today. So far, none have followed through.

Unsurprisingly, there has been pushback from card issuers.

JPMorgan CEO Jamie Dimon said it would be an economic disaster. In short, they’ll argue that a hard cap would force one of two outcomes: They’d either stop offering credit cards to riskier borrowers because the risk-reward tradeoff isn’t fair or they will be forced to lose money lending to many people.

If Washington forces the headline rate down, issuers will have to pull back on credit limits and reduce credit card rewards.

That’s the industry argument. The missing piece is how much profitability cushion exists before the business becomes unworkable.

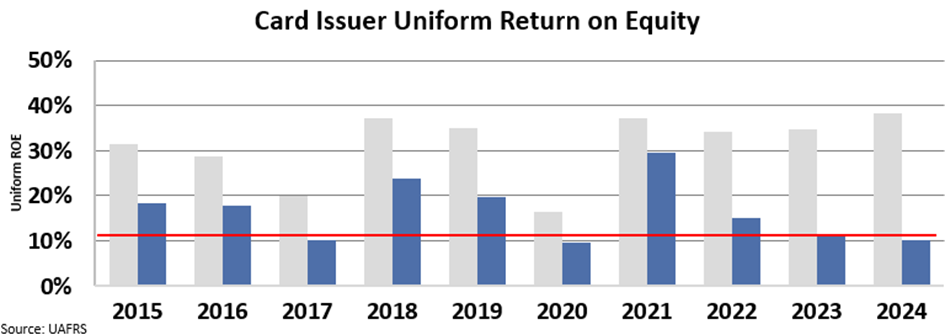

Capital One (COF) and American Express (AXP) are two of the largest card-focused lenders in the U.S., and they have been among the most profitable financial institutions in the public markets.

The average financial institution generates roughly an 11% Uniform return on equity (“ROE”).

Over the past decade, Capital One’s Uniform ROE averaged 17% and American Express averaged over 30%.

Take a look…

Credit card issuers are far more profitable than the average financial institution. That gives credence to Trump’s argument that they have some “wiggle room” to charge consumers less on their credit card bills while still making plenty of cash.

That said, this doesn’t mean the stocks of these issuers won’t take a beating should the proposal push through. A 10% cap is far from certain. Congress would have to act, and even if a limit is imposed, it could be higher than the figure Trump suggested.

That doesn’t mean a 10% cap is painless. It means the debate is happening around a product line that has been priced for maximum profitability, and that leaves more slack than the industry’s messaging suggests.

That said, there’s a clear correlation between the interest rates card issuers can charge and some of the highest profits in the financial sector. For the time being, the safe thing to do is be cautious of major card issuers. They have a lot to lose from this discussion and not much to gain.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.