The March 2026 spending data was stronger than expected.

By March 31, the national average gasoline price had climbed above $4 per gallon for the first time since 2022.

Many expected that shock to hit households fast.

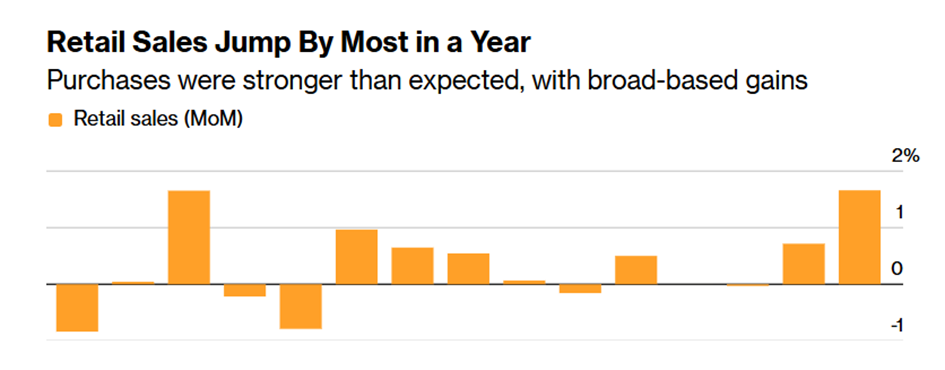

Instead, March retail and food services sales jumped 1.7% to $752.1 billion after a revised 0.7% gain in February. It was the biggest monthly increase in a year, and at first glance it looked like proof the consumer was holding up far better than feared.

However, there’s more to that story than the numbers let on.

The first thing to understand is that March’s retail report was measured in dollars spent, not inflation-adjusted.

Inflation, for the record, jumped to 3.3%, up from 2.4% in February. Not to mention, most of the extra March spending was led by a record jump in gas-station spending.

A jump at the pump does not automatically mean households are feeling flush. Gasoline is one of the most unavoidable line items in a family budget, so when fuel costs rise sharply, spending can climb even as financial flexibility shrinks.

That said, the report was broader than a simple fuel story. Excluding gas stations, retail sales still rose 0.6% in March. Nearly every major category moved higher, including furniture, electronics, and general merchandise.

The so-called control group, which feeds directly into GDP calculations, rose 0.7%, its strongest gain since August. Those numbers show households kept opening their wallets across much of the retail economy.

Still, the strongest conclusion here is moderation. Receipts at restaurants and bars rose only 0.1% in March.

There’s another issue at hand for March, namely that it’s the start of the annual tax refund season.

IRS data through March 27 showed the average refund at $3,521, up 11.1% from a year earlier.

That helps explain why spending showed up in categories far beyond fuel. Bank of America Institute found early filers tended to spend their refunds on anything from debt repayments to electronics.

It’s no surprise last March had the same uptick.

Take a look:

In other words, March’s retail rally may be temporary. And this is why investors should remain wary of the consumer story today.

March was strong enough to calm the most immediate economic fears. But the composition of spending still looks defensive and seasonal. Gasoline and refund money supported what may otherwise have been a weak month.

This report does not offer an all-clear signal for consumer stocks. It argues for patience.

Investors should watch the next few months of oil prices and ex-gas retail sales. If those measures stay firm after the refund season passes, the consumer story gets much stronger.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research