The U.S. healthcare system constantly juggles accessibility, affordability, and sustainability, with Medicaid and Medicare as essential yet complex pillars. Despite its proven record, Universal Health Services (UHS), a major player in the industry, is feeling the weight of shifting policies and reimbursement uncertainties. In today’s FA Alpha Daily, we explore the policy risks shaping investor sentiment and their impact on UHS’s outlook.

FA Alpha Daily

Powered by Valens Research

Last week, we discussed Molina Healthcare (MOH), a giant in the healthcare space that, despite appearing undervalued on the surface, faced significant market skepticism.

The company’s reliance on Medicaid and Medicare, two programs deeply influenced by government policy, left investors worried.

Healthcare in America has long been a balancing act between accessibility, affordability, and sustainability.

Medicaid and Medicare, the two largest government-sponsored programs, are central to this system and offer vital lifelines to millions of Americans.

Medicaid primarily supports low-income individuals, while Medicare focuses on the elderly and disabled.

Despite their importance, these programs face ongoing challenges that affect both patients and providers.

Reimbursement rates, which dictate how much doctors and hospitals are paid for their services, vary widely depending on state policies.

States with lower reimbursement rates often see fewer physicians willing to participate in Medicaid, leaving patients with limited options despite having insurance.

For healthcare providers, these gaps in reimbursement create financial strain, especially for practices in rural and underserved areas.

Universal Health Services (UHS), like Molina, is also struggling…

The company operates a broad network of acute care hospitals, outpatient facilities, and behavioral health centers, with a portfolio spanning 361 inpatient facilities and 49 outpatient facilities across 39 states.

Over the years, Universal Health has shown steady revenue growth. Revenue for 2023 rose by 6.6%, reaching $14 billion, driven by strong performance in both the Acute Care Hospital Services and Behavioral Health Care Services segments.

Acute Care Hospital revenue increased by 5.7%, supported by a rise in inpatient admissions and higher occupancy rates, which improved from 63.7% to 66.2%.

Behavioral Health Care revenue grew by 8%, benefiting from increased patient volumes and higher net revenue per admission.

However, profitability has not kept pace. While net income rose from $675 million in 2022 to $717 million in 2023, operating margins remain below pre-pandemic levels.

The potential for changes in federal healthcare policies poses a significant risk to Universal Health.

Adjustments to Medicare and Medicaid reimbursement rates could impact both the Acute Care and Behavioral Health segments.

These programs are critical revenue drivers, and any unfavorable policy changes could pressure margins further and hinder growth.

This uncertainty has kept investors cautious, despite the company’s recent financial improvements.

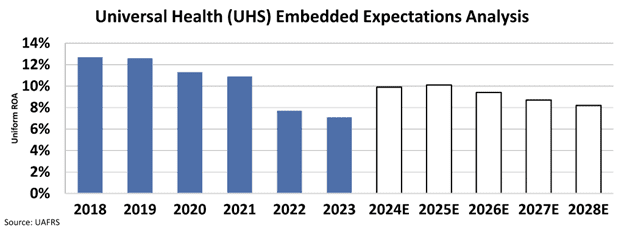

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Despite Universal consistently delivering a strong Uniform return on assets ”ROA”, averaging 13% before the pandemic, the market is pricing the company to have 8% ROA going forward.

Medicare has faced systemic issues for years, including annual payment cuts to physicians.

Since 2021, doctors have seen their reimbursements reduced repeatedly, with another 2.8% cut proposed for 2025. Adjusted for inflation, Medicare payments to physicians have dropped 29% since 2001.

This creates a strain on healthcare providers, especially in underserved areas, and indirectly affects companies like Universal Health that rely on these networks.

One of the main drivers of these cuts is Medicare’s budget-neutrality rules. While intended to keep spending in check, these rules often result in large payment redistributions that hurt providers.

For Universal Health, these policies add another layer of risk, as lower payments to doctors and healthcare providers can disrupt access to care for its members.

At the same time, the healthcare system is moving toward value-based care, where providers are rewarded for quality rather than volume.

While this shift is positive in the long term, it brings new challenges. Providers need better data and infrastructure to meet these goals, which can create costs and uncertainties for companies like Universal Health as they adapt to these changes.

The market’s concerns about the future of the company are valid given the uncertainties surrounding healthcare policies.

Until there is more clarity on potential changes under the Trump administration, particularly regarding Medicare and Medicaid, investors should approach Universal Health with caution.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s highlight, Universal Health Services (UHS) is one of the top stock picks from FA Alpha 50 this month. To see more stock picks like this, become an FA Alpha get access to FA Alpha 50.