School districts are gearing up to replace aging buses, and Blue Bird (BLBD) is leading the charge. As the top player in electric and propane-powered school buses, it’s capitalizing on a fleet nearing retirement and billions in federal funding. In today’s FA Alpha Daily, we explore how Blue Bird is turning this massive replacement wave into a powerful growth engine.

FA Alpha Daily

Powered by Valens Research

In the public sector, the replacement cycle is often based on minimizing costs and maximizing qualities like safety and security.

While products like textbooks can sometimes be delayed practically indefinitely, school buses are another story.

With school buses, there are a few important factors to consider…

First, they are used to transport children, so safety is a top priority. Older buses aren’t going to have the same safety standards as newer models, so there’s very little margin for delaying school bus replacement.

Additionally, there are fuel costs to consider. Older buses will have older, less efficient engines and will therefore have higher variable costs over their useful lives.

Most states set 15 years as a replacement target age for their bus fleets. That’s why it’s important to note that more than 47% of the school buses on the road currently are 10 years old or older.

Looking closer, we can see that before the pandemic, there was an average of 31,000 school buses ordered every year.

But in the past three years, significantly fewer were ordered. An aging school bus fleet means a lot of replacements can be expected soon.

This is where Blue Bird (BLBD) comes into play. It is one of the three big school bus makers that collectively own around 95% of the market.

Of the other two, Thomas Built is owned by Daimler, which is owned by Mercedes-Benz (DMLRY), and IC Bus is owned by Navistar, which is owned by Volkswagen (VWAGY).

As such, Blue Bird is the only pure-play bus maker and the only way to get exposure to the bus replacement cycle.

Blue Bird is also the clear leader in alternatively fueled buses, which makes it even more interesting for investors.

While it’s in a dead heat with the other big players for total buses sold, it’s the No. 1 seller for propane and electric buses, and since 2015, Blue Bird has increased its alternative power mix from just 17% of buses sold to 60% in 2024.

It’s moving aggressively into the electric vehicle (“EV”) market, and as of 2024, Blue Bird owned more than 60% of the EV bus market, up from less than 30% before the pandemic.

This is a major tailwind. Policies like the CLEAN Future Act, along with a $5 billion boost from the U.S. government for school bus electrification, allocate billions of dollars toward EV bus spending over the coming years.

Buses are a smart place for EV technology because bus routes have predictable, fixed driving ranges on any given day.

While fixed ranges are often seen as a disadvantage of cheaper-to-operate electric vehicles, municipalities will be able to leverage this to their advantage and reap the benefits of moving to electric vehicles.

While the pent-up demand already started to show up in the company’s income statement, there will be more bus demand to replace the oldest buses in the near term, and many more municipalities may be exploring EV options today than there would have been three years ago.

Blue Bird isn’t just a way for investors to get direct exposure to a powerful replacement cycle. Because it has the biggest exposure to EVs, it could actually pull ahead of its peers.

Furthermore, while investors might be concerned that Blue Bird is a manufacturing firm in an inflationary environment, the company is also in the process of implementing a variable pricing model for its multiyear contracts that move with inflation, significantly mitigating this risk.

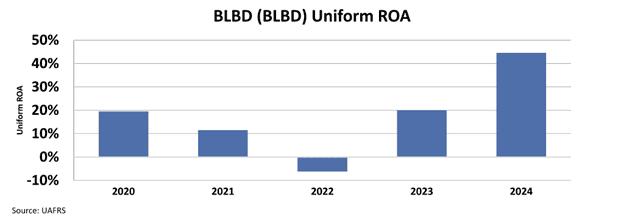

All these factors combined enabled the company to achieve a 45% Uniform return on assets ”ROA” last year.

And yet, the market doesn’t seem to understand just how powerful this could be for the company.

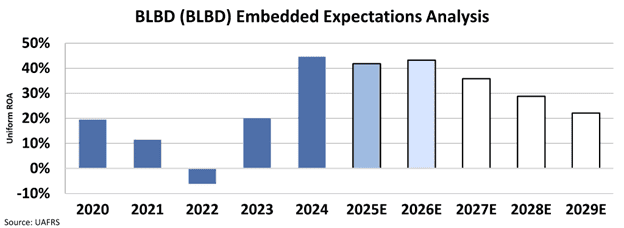

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s Uniform ROA to decline to around 22% from 45% last year.

Considering what Blue Bird has achieved before, it can stay as a 40% ROA business as the bus replacement efforts surge.

All the data say we’re heading for a positive replacement cycle for school buses with a tilt toward electric buses, and Blue Bird is the most directly exposed to benefit from this cycle.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.