Activist investors are dialing up the pressure on Victoria’s Secret (VSCO) after years of underperformance and failure to adapt to evolving consumer tastes. Since its 2021 spinoff, the stock has lost over half its value, prompting calls for leadership changes and a strategic overhaul. In today’s FA Alpha Daily, we explore how operational missteps, external headwinds, and investor unrest are converging to force a critical turning point for the brand.

FA Alpha Daily

Powered by Valens Research

Activist investing represents a strategy aimed at companies that have notably underperformed their peers or the broader market.

Investors employing this approach take significant minority stakes in these businesses with the clear goal of influencing management to enact specific changes that will unlock shareholder value.

The core of this strategy is to identify the root causes of a company’s persistent underperformance and then propose concrete strategic, financial, or operational adjustments.

This can range from altering a company’s strategic direction and improving its management to optimizing how capital is allocated.

In some cases, activists may push for a company to use its excess cash to increase dividends or buy back shares, thereby directly returning value to shareholders.

The ultimate objective is to create a catalyst that closes the gap between a company’s current stock price and its potential intrinsic value.

Women’s apparel retailer Victoria’s Secret (VSCO) is facing intense pressure from activist investors who are demanding a significant corporate turnaround.

These investors are questioning the effectiveness of the current management, arguing they have failed to steer the company in a profitable direction.

Their complaints are pointed, and after looking at Victoria’s Secret’s recent track record, it’s hard to dismiss them as overreactions.

Since being spun off from L Brands in 2021, the company’s stock has dropped more than 50% while the S&P 500 has soared.

This underperformance is not just about the numbers. Victoria’s Secret has been slow to adapt to a changing customer base, one that no longer responds to the outdated “perfect body” image that once defined the brand.

Competitors like Skims and Savage X Fenty have capitalized on the shift toward inclusivity and comfort, capturing younger audiences with more relevant messaging and products.

While VSCO once generated nearly $8 billion in sales at its peak under L Brands in 2016, it closed 2023 at $6.2 billion and only slightly improved to $6.23 billion in 2024.

That’s not the trend you want to see if you’re betting on a turnaround.

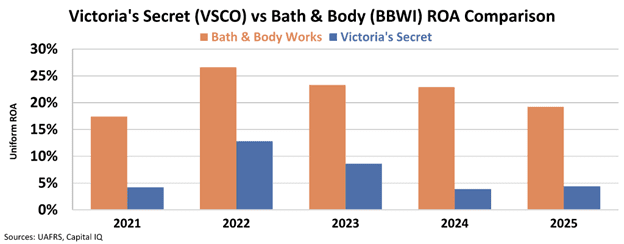

The company’s performance since its 2021 spinoff from L Brands further illustrates the investors’ worries.

While the former parent company, now Bath & Body Works (BBWI), has maintained a Uniform return on assets ”ROA” of over 20%, Victoria’s Secret’s returns have plummeted to below 5%.

The scrutiny has intensified recently with activist firms Barington Capital Group and BBRC International publicly voicing their intentions.

In just over a week, both have criticized the company’s CEO and board chairman for what they term the destruction of shareholder value and a failure to implement a successful business turnaround.

BBRC International, led by Australian billionaire Brett Blundy, has specifically targeted Board Chairman Donna James, questioning her 20-year tenure and calling for her immediate removal to allow for a refreshed board.

BBRC has also been critical of what it deems continued mismanagement, pointing to a recent “security incident” that forced the company to shut down its website and delay its first-quarter results release.

BBRC contends this could have been avoided with better oversight and expects substantive responses from the board.

In response to the mounting pressure, particularly from BBRC’s growing stake of around 13%, Victoria’s Secret adopted a “poison pill” shareholder rights plan in May to prevent a hostile takeover.

This move, however, has been criticized by Barington Capital as a negative signal to the market that could deter valuable propositions.

Barington, holding just over a 1% stake, has echoed the call for a board overhaul, insisting on directors with experience in brand revitalization and operational efficiency.

They argue that the current board has overseen a $2.4 billion destruction in shareholder value while approving $1.8 billion in capital expenditures with little to show for it.

And the market agrees with the concerns of these investors…

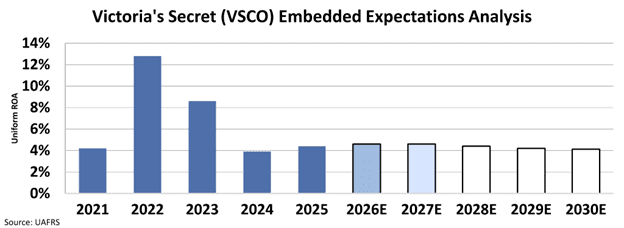

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s Uniform ROA will stay around 4%, below the cost of capital.

On top of all this, there are external headwinds to manage. The company was recently hit with a cyberattack that shut down its website and delayed quarterly earnings. The fallout from that incident is expected to cost about $10 million.

Add another $50 million in expected tariff-related expenses for FY25, and the pressure on near-term performance is clear.

These costs are front-loaded, so even if mitigation efforts are underway, investors are still staring down weaker results for at least the next couple of quarters.

Valuation isn’t compelling enough to absorb all this risk. The stock trades around 20x forward Uniform earnings, which is roughly in line with peers like Gap (GAP) and American Eagle (AEO).

That might seem reasonable, but if Victoria’s Secret continues to show weakness in its core categories, the multiple could compress sharply.

Without evidence of real momentum in its turnaround and with activist pressure ramping up, it’s hard to make the case that this is a buying opportunity.

Victoria’s Secret may stabilize eventually, but right now, it’s stuck in the middle of too many unresolved issues.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.