Mission-critical infrastructure such as specialized medical facilities, factories, data centers, scientific laboratories, and the likes need reliable mechanical, electrical, plumbing, and controls (“MEPC”) systems to run safely and efficiently on a daily basis.

Companies like Limbach Holdings (LMB) play a crucial role in supplying the complex construction and engineering needs of these mission-critical facilities.

Limbach is a building systems solutions company that specializes in custom engineering solutions for MEPC systems.

The company’s custom solutions include integrated facility planning, service and maintenance, infrastructure upgrades, replacements and retrofits, rental equipment, and energy efficiency and decarbonization.

Limbach currently services a diverse range of sectors such as healthcare, industrial and manufacturing, data centers, life sciences, higher education, and culture and entertainment.

Limbach generates its revenue through two operating segments, namely owner direct relationships (“ODR”) and general contractor relationships (“GCR”). In 2020, the GCR segment delivered 78% of the company’s revenues.

GCR projects were typically one-off engagements where Limbach was only tapped to provide its services on a per-project basis. Since this demand is cyclical, the company was vulnerable to construction cycle vulnerability.

And that’s why Limbach slowly shifted towards ODR, since it enabled the firm to work with customers directly and allowed it to leverage its engineering and construction expertise to provide recurring and long-lasting custom solutions to building owners.

In 2020, ODR comprised only 22% of Limbach’s revenues. Fast forward to 2025, that number has risen to 75%.

The ODR segment derives its revenue through a combination of fixed-price projects (73%) and recurring maintenance contracts (27%). Moving forward, the company’s management expects this segment to generate between 75% to 80% of the company’s total revenue.

Limbach’s aggressive shift towards ODR has significantly improved its business’ quality. Unfortunately, investors continue to underestimate this company.

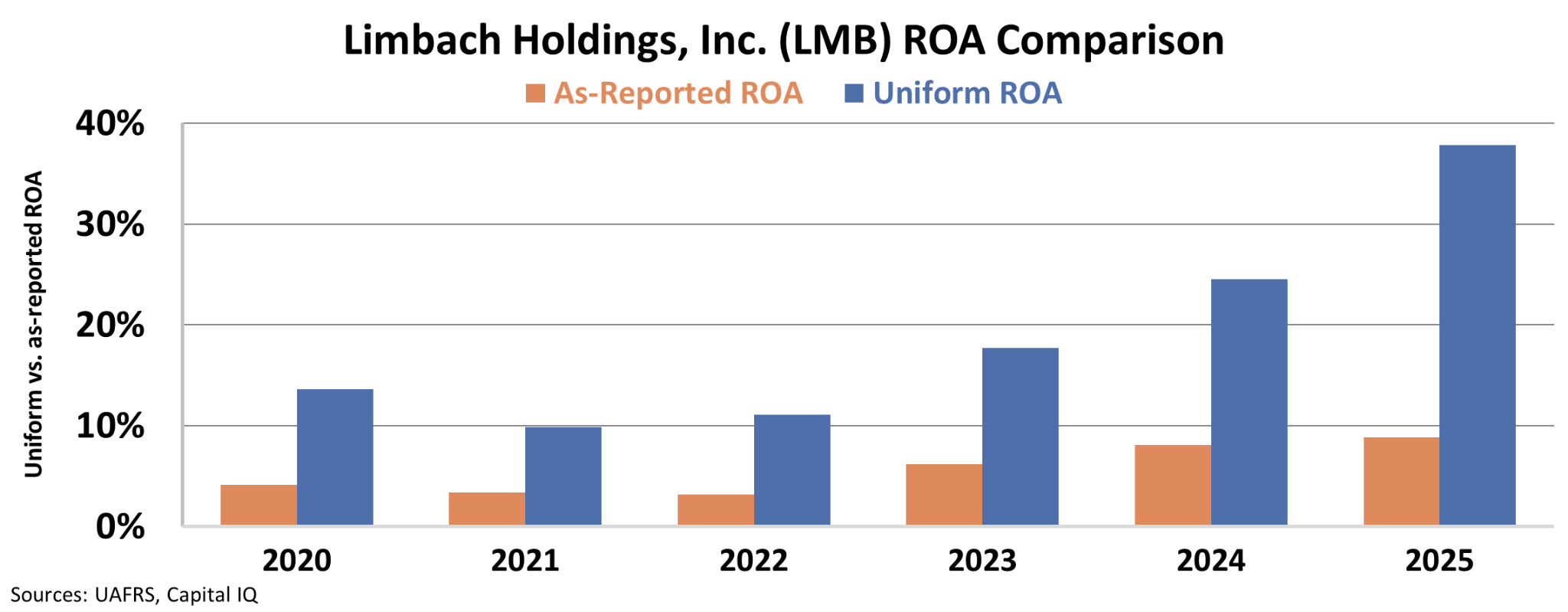

The company’s as-reported return on assets (“ROA”) has doubled slightly from 4% in 2020 to 9% last year, below the 12% corporate average.

However, when viewed through the lens of Uniform Accounting, the improvements Limbach has made to its business becomes more apparent.

Limbach’s Uniform ROA has climbed steeply from 14% in 2020 to 38% in 2025.

Investors who rely on as-reported numbers haven’t been able to see just how profitable Limbach has been. Instead of seeing an above-average business, what they see is a below-average firm.

With Limbach’s transformation, business model, and focus on servicing mission-critical infrastructure, it’s positioned to support and grow its high returns for years to come.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.