Rapid advances in AI are fueling concerns that software automation could weaken the cybersecurity industry’s traditional advantages. Yet the same technology that accelerates threat detection is also making cyberattacks more complex and difficult to manage. In today’s FA Alpha Daily, we examine why companies like Qualys (QLYS) may become even more important in an AI-driven security landscape and what the market could be overlooking.

FA Alpha Daily

Powered by Valens Research

Rapid advancements in AI have brought anxiety to investors exposed to tech and software stocks.

Much of this sentiment is rooted in fears that AI will make software solutions and software vendors obsolete due to automation. The S&P Software Index is still down roughly 15% year-to-date,

Unfortunately, this anxiety has made its way to cybersecurity stocks as well.

A few months ago, AI leader Anthropic rolled out a new AI model called Claude Mythos Preview. The company claimed the model can pinpoint and identify cybersecurity vulnerabilities at a scale that far outpaces human capacity.

The model was reported to have found thousands of previously undiscovered zero-day vulnerabilities and other flaws.

In one case, the model uncovered a flaw in popular video software that went undetected for 16 years. The vulnerable line of code had already been executed 5 million times by automated testing tools without getting flagged.

Claude Mythos’ capabilities are so potent that only select companies like Amazon (AMZN), Apple (AAPL), Microsoft (MSFT), Cisco (CSCO), CrowdStrike (CRWD), and others have been given access.

Much of the cybersecurity industry is built around human experts spotting blind spots and helping companies respond once something goes wrong. If an AI model can surface hidden flaws faster than human teams and legacy tools, investors would have to rethink how they view the industry as a whole.

That said, AI advancement cuts both ways. As AI models become more adept at exploiting vulnerabilities, the more indispensable cybersecurity firms will become in detecting attacks, managing risk, and ensuring compliance.

And one of the companies that brings all those to the table is Qualys (QLYS).

Qualys is an information technology (“IT”) SaaS firm specializing in cybersecurity solutions for small and mid-sized businesses, enterprise, federal, and managed service provider (“MSP”) customers.

When Anthropic first introduced Mythos, investors feared Qualys was at risk of obsolescence.

The stock dropped more than 13% in just two trading days… and is now down roughly 25% year-to-date. But the market may be looking at this the wrong way.

While Mythos is adept at identifying potential risks, one key for cybersecurity is understanding which risks actually matter, and fixing them before attackers can act.

Qualys’ flagship offering, the TruRisk Platform, solves this problem. TruRisk evaluates vulnerabilities in real-world context, considering which systems are exposed to the internet, which assets are critical, which threats are active, and what protections are already in place.

Most vulnerabilities don’t pose immediate danger, Qualys helps identify which risks are worth a security team’s time and effort to resolve. Its TruConfirm tool tests whether a vulnerability can actually be exploited, safely simulating an attack without disrupting operations. Once a risk is confirmed, Qualys can fix it quickly. Its TruRisk Eliminate platform automates remediation across patches, configurations, and system changes.

The company has deployed tens of millions of automated patches with minimal failures and almost no need for manual intervention. As AI makes vulnerability discovery faster the need to prioritize and fix risks becomes even more urgent. That dynamic should benefit Qualys – not hurt it.

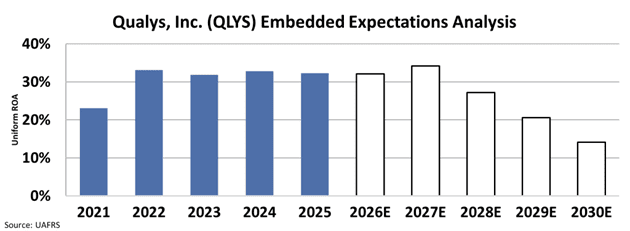

Still, investors are doubting the future for this business. We can see this through the Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what investors expect from future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At current valuations the market believes that Qualys’ Uniform return on assets (“ROA”) will decline from 32% in 2025 to just 14% by 2030, along with 7% asset growth going forward.

Qualys has generated a Uniform ROA of roughly 32% to 33% for four straight years, nearly three times the corporate average. Growth has been solid as well. Uniform asset growth has averaged 19% over the past five years.

This disconnect has pushed the stock to an all-time low 12x Uniform P/E, well below the market average of 20x.

For a business with stable profitability, recurring demand, and increasing relevance in an AI-driven world, that valuation stands out.

As cybersecurity shifts toward machine-speed decision-making, Qualys is positioned to play an even more critical role. The market’s recent fears may have created an opportunity.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research

Today’s analysis highlights the same insights we share with our FA Alpha Members. If you want to an get in-depth analysis of market trends and uncover undervalued stocks, become an FA Alpha Member today.